From 1 January 2026, every employer in Ireland must automatically enroll eligible employees into My Future Fund and match their pension contributions. This applies regardless of business size. There is no minimum headcount threshold, auto enrolment Ireland small business obligations are identical to those of large employers.

The auto-enrolment pension scheme is governed by the Automatic Enrolment Retirement Savings System Act 2024 and administered by the National Automatic Enrolment Retirement Savings Authority (NAERSA). Using Revenue payroll data, NAERSA identifies eligible employees, manages enrolment records and oversees the collection and administration of pension contributions within the central retirement savings system.

Contributions became a legal obligation from January 2026. If you have not registered or updated your payroll, those contributions are accumulating as a legal debt from that date.

Key Takeaways

- Every Irish employer must register on the MyFutureFund portal using ROS credentials. Not registering does not pause the obligation it creates an accumulating debt to NAERSA.

- NAERSA identifies eligible employees automatically through Revenue. Your responsibility is to keep your Revenue payroll records accurate and submitted on time.

- Auto enrolment contributions start at 1.5% of gross salary for both employer and employee, capped on annual earnings of €80,000.

- Employer obligations under the 2024 Act carry fines of up to €50,000, potential imprisonment and public listing by NAERSA for non-compliance.

Which employees need to be enrolled?

Not every employee qualifies for Auto Enrolment pension scheme in Ireland. NAERSA checks three conditions simultaneously before enrolment begins.

- Aged between 23 and 60

- Earning €20,000 or more per year

- Not already contributing to a qualifying pension scheme through payroll

NAERSA assesses auto enrolment qualifying earnings using a rolling 13-week lookback on Revenue data. If gross earnings reach €5,000 in any 13-week period, the employee meets the income threshold.

What this means for new starters:

If someone joins mid-year and their salary annualises above €20,000, NAERSA identifies this through your Revenue submissions. Employers do not initiate enrolment manually.

However, if payroll data for that employee is submitted late or contains errors, the enrolment will be delayed or incorrect and the liability rests with you. Submit accurate data for every new starter on or before their first payday.

Directors who pay PRSI as employees and meet the criteria must be enrolled. Self-employed directors not paying PRSI as employees are excluded. For employees with multiple jobs, NAERSA assesses combined earnings across all employments.

Each employer enrolls and contributes independently there is no deduction for contributions made elsewhere. Employees should notify NAERSA if duplicate enrolments occur.

Can employees opt in if they do not meet the criteria?

Yes, employees who do not meet the auto-enrolment criteria can still choose to join My Future Fund voluntarily. This includes employees who are under 23, over 60 or earning less than €20,000 a year.

If an employee opts in, the same contribution structure applies. The employer must match the employee’s contributions and the State top-up of €1 for every €3 saved by the employee also applies.

Employees who want to opt in can do so through the NAERSA portal. Once enrolled, the same rules around opt-out windows, suspension and re-enrolment apply as they do for automatically enrolled employees.

What are the Contribution Rates for Auto-Enrolment?

The rates are split three ways employee, employer and State and increase every three years. The table below shows your employer share at each phase.

| Period | Employee | Employer | State | Total |

|---|---|---|---|---|

| Years 1–3 (2026–2028) | 1.5% | 1.5% | 0.5% | 3.5% |

| Years 4–6 (2029–2031) | 3.0% | 3.0% | 1.0% | 7.0% |

| Years 7–9 (2032–2034) | 4.5% | 4.5% | 1.5% | 10.5% |

| Year 10+ (2035 onwards) | 6.0% | 6.0% | 2.0% | 14.0% |

The State contribution is paid directly into the employee’s My Future Fund account by NAERSA. Employers do not collect or remit the State portion; your payroll obligation covers employee deduction and your matching employer contribution only.

All percentages apply to gross salary. Employer and State auto enrolment contributions are capped at annual earnings of €80,000.

For an employee on €40,000, your employer contribution is €600 in 2026 and rises to €2,400 by 2035.

For ten eligible employees at that salary, the annual employer cost goes from €6,000 today to €24,000 by 2035. Account for these increases in your annual payroll budget now.

Key Auto-Enrolment dates every Irish Employer must know

Understanding the auto enrolment dates that govern your obligations helps you stay ahead of each compliance milestone. Here are the critical dates in sequence:

| Date / Period | What happens? |

|---|---|

| 1 January 2026 | Contributions become a legal obligation for all eligible employees |

| Months 1–6 of enrolment | Employee is fully enrolled, no opt-out permitted |

| Months 7–8 of enrolment | Employee opt-out window opens |

| After month 6 | Employee may apply to suspend contributions for up to 2 years |

| 2 years after opt-out or suspension | Automatic re-enrolment if employee still meets eligibility criteria |

| 2029 | Contribution rates increase to 3% employee / 3% employer / 1% State |

| 2032 | Rates increase again to 4.5% each |

| 2035 | Final rate of 6% employee / 6% employer / 2% State takes effect |

What are your Employer Obligations under Auto Enrolment in Ireland?

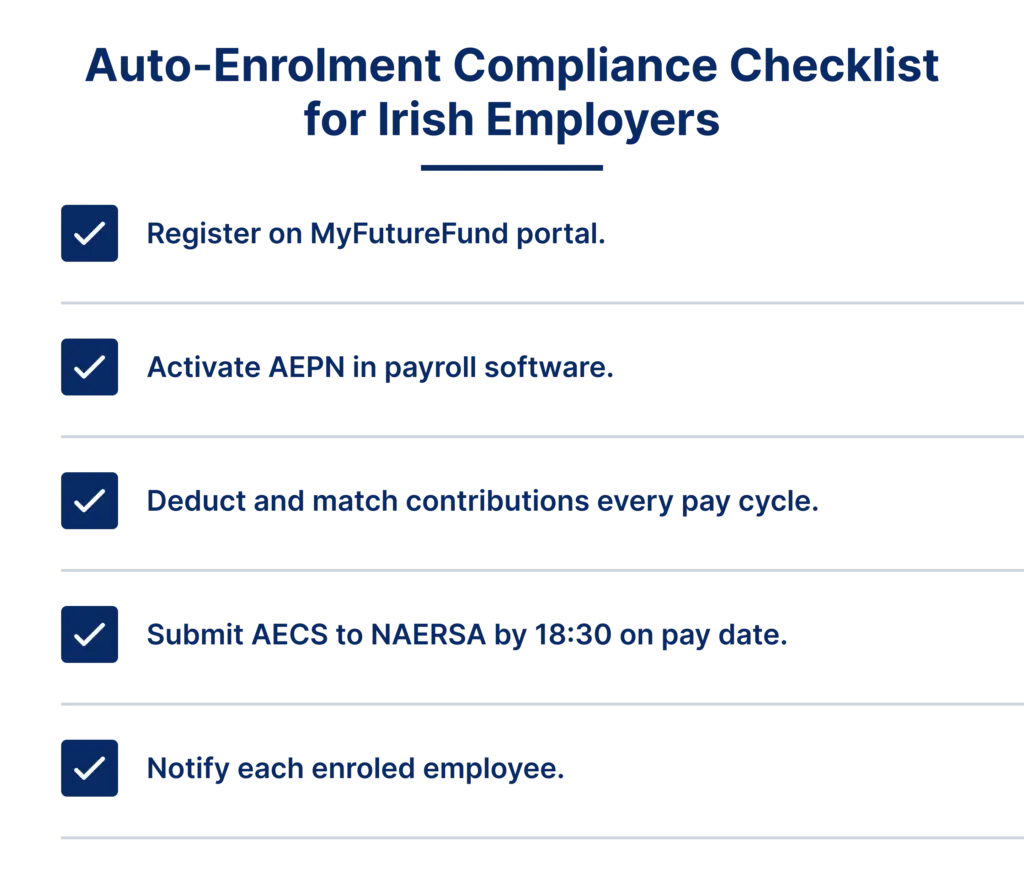

Registration and payroll software must be in place before you can process or submit anything. The checklist below covers the five key employer obligations under auto-enrolment.

These are the main employer obligations under auto-enrolment. Here’s what each one means in practice.

Register on the MyFutureFund portal

Log in at myfuturefund.ie using your ROS credentials, set up your payment method and link your payroll software for AEPN integration. Existing scheme exemptions must also be applied for through this portal; exemption is not granted automatically.

There is no grace period. Contributions owed since January 2026 remain due whether or not you are registered.

Update your payroll software

Your payroll provider must be running the 2026 auto enrolment update. Major Irish providers including BrightPay, Thesaurus Payroll Manager and Sage Payroll have released this update. Confirm with your provider that Automatic Enrolment Pension Notification (AEPN) integration is active before your next payroll run.

Each time you process payroll, the AEPN sends your contribution data directly to NAERSA. Without this update, your payroll cannot communicate with NAERSA. Confirm with your provider that this update is active.

Deduct and match contributions on each payroll

Employee contributions are deducted from net pay. You add your matching employer contribution. Both are submitted to NAERSA through the AEPN on the same payroll.

Submit AECS by 18:30 on pay date

After each payroll run, your payroll software must send an Automatic Enrolment Contribution Submission (AECS) to NAERSA through the AEPN system. This submission must be completed by 18:30 on the employee’s pay date.

Ensure payroll records are accurate before submission, as late or incorrect AECS filings can lead to contribution discrepancies and compliance issues.

Notify every enrolled employee

You must inform each employee when first enrolled, stating their enrolment date, contribution rate and opt-out rights. NAERSA provides standard notification templates through the portal.

Do you already have a Pension Scheme?

Exemption from My Future Fund is not automatic. Your existing scheme must meet a minimum threshold set by the 2025 Regulations, and you must verify this yourself.

If your employees contribute to an occupational pension scheme or PRSA through payroll, they may be exempt.

Under the Automatic Enrolment Retirement Savings System Regulations 2025, in force from 1 January 2026, the exemption requires a total minimum contribution of 3.5% with at least 1.5% funded by the employer.

- If your scheme meets the threshold: Those employees remain exempt and do not need to be enrolled in My Future Fund.

- If your scheme falls below the threshold: Those employees must be enrolled in My Future Fund immediately. You have two options: increase contributions on your existing scheme to meet the 3.5% minimum and seek exemption from NAERSA or enroll the affected employees in My Future Fund and run both schemes alongside each other.

NAERSA is currently conducting its review of existing pension arrangements using payroll data submitted to Revenue. If you have not yet verified your scheme’s compliance, review your contribution levels immediately and contact NAERSA through the MyFutureFund employer portal via your ROS credentials.

What happens when an employee opts out or suspends contributions?

Employees have three possible actions after enrolment: opt out, suspend or be re-enrolled. Each one creates a distinct payroll obligation.

Opt-out (months 7 and 8 only)

Once an opt-out is submitted, your payroll must stop all deductions from the next pay cycle after the opt-out date. If deductions continue past that date, the employee is owed a full refund within the same or next pay cycle, and your payroll is non-compliant. Your 2026 payroll software should flag this automatically.

Suspension (after month 6, for up to 2 years)

When an employee suspends contributions, your employer contributions stop at the same time. Your payroll must reflect this from the correct date not from the following month.

Re-enrolment (after 2 years)

Employees who opted out or suspended are automatically re-enrolled after two years if they still meet the eligibility criteria. Deductions must resume from the correct date. If your payroll software does not monitor re-enrolment dates, set up a separate record to track this.

You cannot pressure or obstruct any employee from joining, remaining in or re-joining the scheme. The Workplace Relations Commission handles complaints from employees penalised for participating in auto enrolment Ireland.

What are the Penalties for Non-Compliance?

The 2024 Act does not distinguish between employers who were unaware and those who deliberately avoided their obligations. The penalties apply in both cases.

- Withheld or underpaid auto enrolment contributions attract interest from the date they were due.

- Fixed-penalty offences carry fines of up to €5,000.

- Serious offences, including blocking enrolment or forcing opt-outs, carry fines of up to €50,000 and/or up to three years imprisonment.

- NAERSA publishes a public list of employers convicted of non-compliance.

Conclusion

Auto-enrolment in Ireland is now part of every employer’s payroll responsibilities. From January 2026, each payroll cycle includes contribution calculations, AEPN submissions, opt-out processing and accurate record processing.

These tasks need to be managed correctly, along with your regular PAYE, PRSI and USC payroll duties. Reviewing your payroll software and pension setup now can help you avoid mistakes, delays and compliance issues later.

If you need support, Outbooks is an Irish payroll service provider offering payroll outsourcing services for businesses of all sizes, covering auto enrolment contributions, NAERSA submissions and full ongoing compliance. Contact us at info@outbooks.com or call +353 212069255.

FAQs

What is auto-enrolment Ireland?

My Future Fund is Ireland’s new state-run auto enrolment pension scheme that automatically enrols eligible employees and requires matching contributions from employers and the State from January 2026.

What is NAERSA Ireland?

NAERSA is the National Automatic Enrolment Retirement Savings Authority, the public body that administers My Future Fund, identifies eligible employees and collects contributions.

What happens if an employer does not comply with auto-enrolment Ireland?

Fines of up to €50,000, potential prosecution and public listing by NAERSA. Unpaid auto enrolment contributions accrue interest from January 2026.

Can employees opt out of auto-enrolment in Ireland?

Only during months seven and eight of enrolment. Employees who opt out are automatically re-enrolled after two years if still eligible.

Is auto-enrolment the same as PAYE Modernisation in Ireland?

No, PAYE Modernisation covers income tax, USC and PRSI reporting to Revenue. Auto enrolment is a separate pension contribution system managed by NAERSA.

How do auto-enrolment contribution rates work in Ireland?

Employee and employer each contribute 1.5% of gross salary in 2026, with the State adding 0.5%. Rates increase every three years, reaching 6% each by 2035.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.