Payroll in Ireland became more complex from 1 January 2026, when My Future Fund introduced a new set of auto-enrolment obligations for employers. Payroll teams now must manage additional pension related tasks during every pay run: including new NAERSA notifications, contribution processing and stricter remittance requirements.

Most businesses were already managing PAYE, PRSI, USC and Enhanced Reporting Requirements. The new payroll framework has added another compliance layer and for many employers, especially in retail, hospitality and care services managing payroll has become far more complex.

This blog explains what changed under Ireland’s auto-enrolment scheme, why many employers are finding it difficult to manage internally and how payroll outsourcing can help reduce pressure.

Key takeaways

- Payroll software must retrieve the latest Automatic Enrolment Payroll Notification (AEPN) from NAERSA at every pay run. A new AEPN is issued only when an employee’s status changes, enrolment, opt-out, suspension or rate change.

- Contributions and the Auto-Enrolment Contribution Submission (AECS) must reach NAERSA by 18:30 on the pay date, making payroll processing and pension payments a single coordinated process.

- To qualify for exemption from MyFutureFund, a defined contribution pension scheme must provide at least 3.5% of gross pay in total contributions, including at least 1.5% from the employer (up to €1,200). Schemes below these limits may require running two separate contribution processes.

- NAERSA publishes a public register of employers convicted of non-compliance, so errors carry reputational consequences beyond any financial penalty

Why are Irish Employers choosing to Outsource Payroll?

The main reasons are higher workload, more complex rules and employee eligibility changing during the year.

1. The workload has increased for in-house teams

Before January 2026, payroll in Ireland was already carrying a heavy compliance load following PAYE Modernisation, Real-Time Reporting, Enhanced Reporting Requirements and Statutory Sick Pay updates. Each of those changes required software updates, staff retraining and process changes.

Auto-enrolment did not replace any of that. It added to it. AEPN processing, dual-system pension management and continuous eligibility monitoring now sit on top of everything that was already there. For businesses with small payroll teams, keeping up with all of it has become genuinely difficult.

2. Eligibility changes throughout the year

An employee is eligible for auto-enrolment if they are aged between 23 and 60, earn €20,000 or more per year and are not already in a qualifying pension scheme. That threshold is assessed over a reference period of up to 13 weeks, not against an annual salary figure.

A part-time worker whose hours increase, a new starter or someone returning from a gap in employment can each become eligible at different points in the year. For businesses with seasonal or variable workforces, that list shifts constantly and tracking it manually inside a busy payroll function is where errors tend to happen.

3. The dual-system problem

Where an existing pension scheme does not meet the exemption standards, affected employees may still need to be enrolled through NAERSA.

For defined contribution occupational pension schemes, total contributions must amount to at least 3.5% of the employee’s gross pay, of which at least 1.5% must be made by the employer, subject to a maximum of €1,200, to exempt an employment from enrolment in MyFutureFund.

Employers whose schemes fall short of either element may find themselves running two separate contribution processes within a single pay cycle. For smaller businesses, that is a meaningful additional burden on every pay run.

The Benefits of Outsourcing Payroll Services in Ireland

Moving to a managed payroll service changes more than just who handles the admin. It also changes how payroll is managed in practice.

The key advantages include:

- Reduced compliance risk: AEPN retrieval, NAERSA submissions, eligibility monitoring and remittance timing are all handled by the provider. Missed contributions, late submissions and incorrect eligibility decisions carry penalties under the current framework. Outsourcing reduces that risk without adding to your internal workload.

- Scalable for variable headcount: For businesses with changing workforce sizes, the service adjusts as employees join, return or cross the €20,000 threshold. New starters and part-time workers are assessed and enrolled as part of the ongoing service.

- Automatic rate updates: The phased contribution schedule is managed by the provider at each step, removing the need to reconfigure internal systems when rates increase.

- Cost efficiency: Adding up payroll software licences, staff training and compliance time often reveals that a managed payroll service cost less per employee than the combined internal spend, before any error or penalty costs are factored in. Request a quote and compare it against your actual spend before deciding.

What has changed in Irish Payroll from 1 January 2026?

Auto-enrolment is often discussed as a pension reform, but for employers its biggest impact has been on day-to-day payroll administration.

From January 2026, employers became responsible for handling additional pension contributions through payroll under the My Future Fund scheme. This includes receiving and applying AEPNs, deducting employee contributions, paying employer contributions and meeting new remittance deadlines.

The AEPN

When NAERSA confirms an employee is eligible, it sends an Automatic Enrolment Payroll Notification (AEPN) through payroll software, informing the employer of the contribution amounts due from both the employer and employee as a percentage of gross earnings.

Payroll must retrieve the latest AEPN at each pay run and apply any updates before employees are paid.

A new AEPN is only issued when something changes for that employee, such as enrolment, opt-out, suspension or a rate adjustment, so not every employee will have a new notification at every cycle.

Portal registration

The NAERSA employer portal opened on 1 December 2025 and registration is mandatory for every employer, regardless of whether staff are already in a pension scheme. Access uses existing ROS credentials and takes only a few minutes.

Contributions become due from the first payroll cycle of 2026, regardless of whether an employer has registered on the portal. Delaying registration does not delay the obligation. It means building up a legal debt and risking compliance action from NAERSA.

Registration is done using ROS credentials and takes only a few minutes. There is no exemption from registration based on whether staff are already in a pension scheme. All employers must register.

Why preparation was difficult?

The regulations setting minimum contribution standards for existing pension schemes were signed by Minister Calleary just before the scheme launched and came into force on 1 January 2026.

To qualify for exemption, a defined contribution scheme must provide total contributions of at least 3.5% of the employee’s gross pay (subject to a maximum of €2,800 per year), with at least 1.5% from the employer (subject to a maximum of €1,200 per year).

Employers who had reviewed their pension arrangements in the months before launch were working from earlier guidance and had to reassess once the final requirements were confirmed just days before the scheme went live.

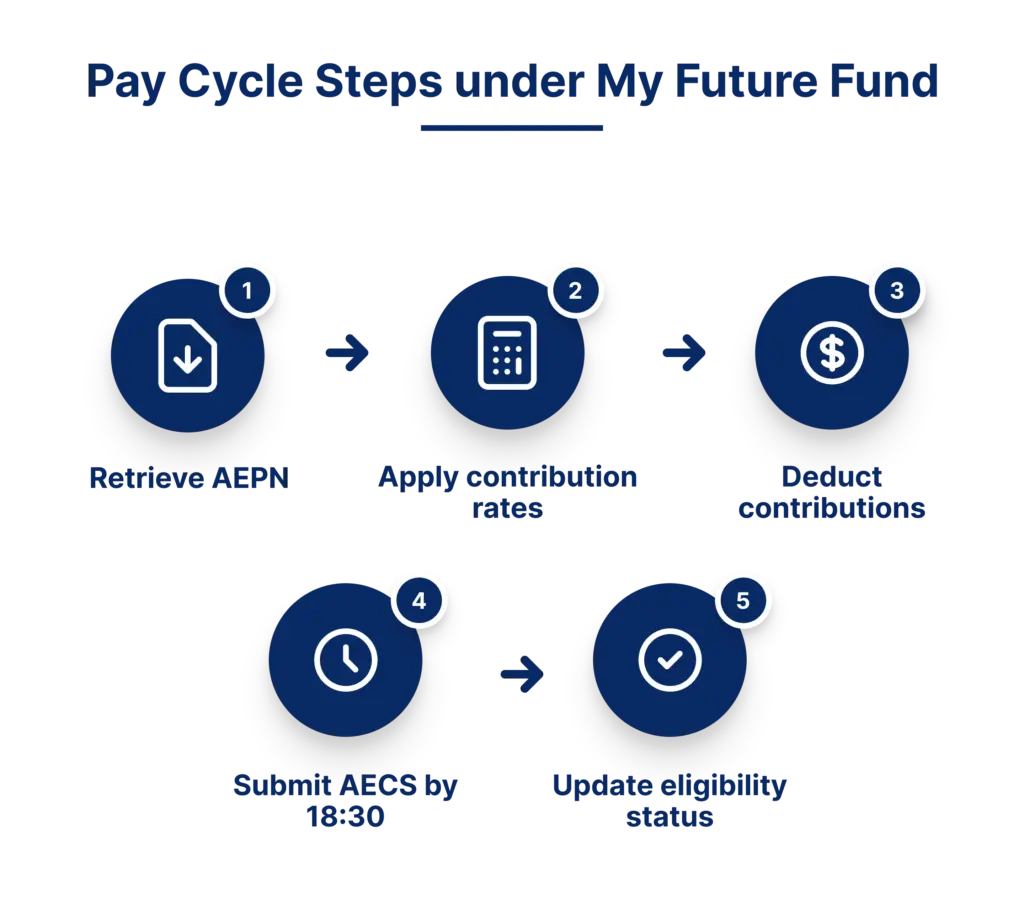

How every pay cycle works after Auto-Enrolment?

Every pay run now follows a fixed sequence of steps that must be completed in the correct order on every pay date.

Each of these steps is a legal obligation. Missing any one of them on any pay date can lead to compliance action from NAERSA. Managing this sequence accurately on every pay date is where a structured payroll process makes the difference. Understanding what that support looks like in practice helps in deciding whether it is the right fit for your business.

What does Payroll Outsourcing in Ireland typically cover?

Payroll outsourcing in Ireland now includes more than routine payroll processing, with many providers supporting auto-enrolment administration as part of their service.

A managed payroll service processes the AEPN each pay cycle, calculates the correct employer and employee contributions and applies them through payroll before remittance. Contributions apply only to gross earnings up to €80,000 a year, once an employee crosses that cap, the AEPN updates and no further contributions are deducted for the rest of the year. For employers managing an existing pension scheme while also meeting auto-enrolment obligations, both contribution processes can be handled separately to help ensure employees are placed in the correct scheme and no deductions are missed.

Eligibility is monitored throughout the year for part-time staff, new starters and variable-hours employees based on the 13-week assessment period. The phased contribution schedule is also updated at each step: 1.5% currently, rising to 3% in year four, 4.5% in year seven and 6% by year ten, removing the need for employers to reconfigure their own systems each time.

What does Non-Compliance under Auto-Enrolment Scheme mean?

The Department of Social Protection is clear that employers who fail to meet their obligations will face penalties and may be prosecuted. Withheld or underpaid contributions may lead to interest charges, increasing the overall cost of the original error.

| Risk | What it means? |

|---|---|

| Penalties and prosecution | Fines up to €50,000 and/or imprisonment up to three years for serious offences, or a Class A fine and/or up to six months for minor offences, under the Automatic Enrolment Retirement Savings System Act 2024, including failure to pay contributions, hindering participation or making false statements. |

| Interest on underpaid contributions | Underpaid contributions accumulate interest, increasing the total cost of the original error |

| Public register | NAERSA publishes a list of convicted employers visible to staff, clients and prospective employees. Entries are removed within two years of the penalty being imposed. |

| WRC complaints | The Workplace Relations Commission handles complaints where employees are hindered from joining, penalised for participating, or pressured to opt out, with awards of up to four weeks’ remuneration plus public reporting. |

| Employee relations | My Future Fund deductions appear on every payslip. A missing or incorrect contribution is visible to the employee on payday |

When should businesses switch to Outsourcing Payroll?

Businesses can switch to outsourcing payroll at any point in the tax year, but preparing the right information helps make the process smoother.

Before switching payroll providers, prepare

- Current payroll records and deductions

- Employee tax and payment details

- ROS and NAERSA login access

- Existing pension scheme details

Many businesses choose to switch at the start of a new pay period. Some providers also run one parallel payroll cycle to check everything before taking over fully, helping ensure payroll continues without disruption.

Conclusion

Auto-enrolment in Ireland is now a permanent part of payroll from 1 January 2026. AEPN retrieval, dual-system pension management and ongoing eligibility checks are built into every pay cycle and do not reduce over time. Contribution obligations and reporting requirements continue to increase in structured phases, making payroll more complex year on year.

For SMEs with limited internal capacity, especially those managing variable or seasonal workforces, payroll outsourcing provides a practical way to maintain accuracy and compliance without increasing internal workload. It helps ensure payroll is processed correctly while reducing the risk of errors under ongoing regulatory pressure.

Outbooks provides payroll outsourcing services covering PAYE, PRSI, USC, ERR and auto-enrolment processing. Support is available for businesses dealing with AEPN handling, eligibility tracking or dual-system payroll management from the next pay cycle.

FAQs

How has auto-enrolment increased payroll responsibilities for Irish employers?

Irish payroll already included PAYE, PRSI, USC and Enhanced Reporting Requirements. Auto-enrolment has added eligibility checks, contribution calculations and NAERSA submissions to every payroll cycle, increasing both workload and compliance responsibilities.

Why is auto-enrolment difficult for businesses with seasonal or variable staff?

With eligibility assessed over a rolling 13-week period, employees with changing hours or seasonal work patterns can become eligible at different times. This makes payroll monitoring more complex and increases the risk of missed enrolments or administrative errors.

What happens if an employer gets auto-enrolment payroll wrong in Ireland?

Incorrect or missed contributions can lead to financial penalties, interest charges and possible legal action. Employers may also face public listing for non-compliance, while employee complaints can lead to compliance checks and increase administrative and reputational risks.

What administrative duties do employers have under auto-enrolment?

Employers must register with NAERSA, monitor enrolment notifications, process contributions correctly and submit payments on time during every pay run. Businesses with non-exempt pension schemes may also need to manage separate pension processes.

How does outsourcing make auto-enrolment payroll easier for businesses?

Outsourcing payroll helps businesses manage the extra work created by auto-enrolment. A payroll provider can handle eligibility checks, contribution calculations, AEPN notifications and NAERSA submissions as part of the payroll process. This reduces compliance risks, lowers the chance of errors and saves time for internal teams.

When should businesses review their payroll process after auto-enrolment?

Businesses should review their payroll process immediately, meaning within the current payroll cycle or at the next one. The idea is to check and validate payroll setup in real time so auto-enrolment contributions, eligibility rules and deductions are working correctly before any future rate increases or compliance changes take effect.

Why are small Irish businesses outsourcing payroll after auto-enrolment?

Auto-enrolment has made payroll more complex and time-consuming for small businesses. Many employers now find that payroll software, staff training and ongoing compliance management cost more in time and resources than using a managed payroll service. Outsourcing helps reduce admin work, lower the risk of errors and keep payroll compliant as contribution requirements continue to increase.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.