Dividends in Ireland aren’t taxed separately; they’re added to your personal income and taxed at your marginal rate. When a company pays you a dividend, it applies the Ireland dividend withholding tax rate of 25% (DWT) at source and remits it to Revenue on your behalf. However, the amount deducted may not cover the full tax you owe on the dividend.

What you actually owe depends on your own tax band. Income Tax, Universal Social Charge (USC) and Pay Related Social Insurance (PRSI) all apply to dividend income, which means higher-rate taxpayers often face a significant balance due at filing time.

In this guide, you’ll find the dividend tax rates for 2026–27, the Budget 2026 changes, examples and exactly how to calculate, report and pay your tax correctly.

Key takeaways

- Ireland has no dividend allowance, so all dividend income is taxed at your normal rate

- Budget 2026 left income tax rates and USC bands unchanged from 2025. The standard rate band for a single person remains at €44,000

- The only 2026 change is PRSI rising by 0.15 percentage points from 4.2% to 4.35% effective 1 October 2026

- Higher-rate taxpayers usually pay more tax than the 25% already deducted and the extra amount is paid through self-assessment

- Standard-rate taxpayers may get a refund if DWT deducted exceeds their actual liability

- Revenue is already informed of all dividend payments made by Irish companies before you file your tax return

How are Dividends Taxed in Ireland for 2026-27?

In Ireland the total income of your dividend and your annual income are added. The total is then charged across three components, Income Tax, USC and PRSI. The rate that applies depends on where your total income falls within each tax band.

Budget 2026 update: Income tax rates and USC bands are unchanged from 2025. The third USC band remains at 3%. The only change taking effect this year is a PRSI increase of 0.15 percentage points from 1 October 2026.

Income Tax Rate Bands for 2026-27:

| Filing Status | 20% Up To | 40% Above |

|---|---|---|

| Single | €44,000 | €44,000 |

| Single parent (SPCCC) | €48,000 | €48,000 |

| Married, one income | €53,000 | €53,000 |

| Married, two incomes | €88,000 combined | Above |

| Income Band | Rate |

|---|---|

| Up to €12,012 | 0.5% |

| €12,013 to €28,700 | 2% |

| €28,701 to €70,044 | 3% |

| Above €70,044 | 8% |

Note: Individuals aged 70 or over, or those holding a full medical card with income not exceeding €60,000, pay a maximum USC rate of 2%.

| Period | Rate |

|---|---|

| 1 January 2026 to 30 September 2026 | 4.2% |

| From 1 October 2026 | 4.35% |

PRSI applies to dividend income for proprietary directors and self-employed individuals with total income above €5,000. PAYE employees on Class A are generally not liable to PRSI on investment income. The minimum annual Class S PRSI contribution is €650.

How does Dividend Withholding Tax work?

Dividend Withholding Tax is not a separate tax. It is a collection mechanism through which the paying company deducts 25% at source and remits it to Revenue on your behalf. The key point is how that amount is treated when you file your return.

How to calculate tax credits on dividends

DWT counts as a tax credit against your final liability, not a separate charge. When you file, you declare the gross dividend (before DWT), calculate your actual liability across Income Tax, USC and PRSI, then apply the DWT already paid as a credit against that total. If the credit exceeds your liability, Revenue refunds the difference. If your marginal rate is above 25%, the remaining balance is paid through self-assessment.

What DWT applies to?

DWT applies to different types of dividend payments, including:

- Cash dividends: Direct cash payments to shareholders from company profits

- Scrip dividends: Additional shares issued instead of cash; these carry a taxable value and are treated as income for DWT purposes

- Non-cash distributions: Benefits, property,or other assets distributed in lieu of money; the paying company calculates and remits DWT on the equivalent cash value

- Close company expenses paid to participators: Where a close company (typically controlled by a small number of people) pays personal expenses for its owners or shareholders, those payments may be treated as distributions and taxed accordingly

Foreign dividends are slightly different. No Irish DWT is deducted at source, but they are still taxable in Ireland at your personal marginal rate under Case III of Schedule D.

Who is exempt from DWT?

Irish resident companies, approved pension funds, qualifying charities and EU parent companies are exempt from DWT. From 1 January 2026, qualifying EEA investment limited partnerships that are equivalent to an Irish Investment Limited Partnership (ILP) are also excluded from the DWT scope, a change introduced under Finance Act 2025.

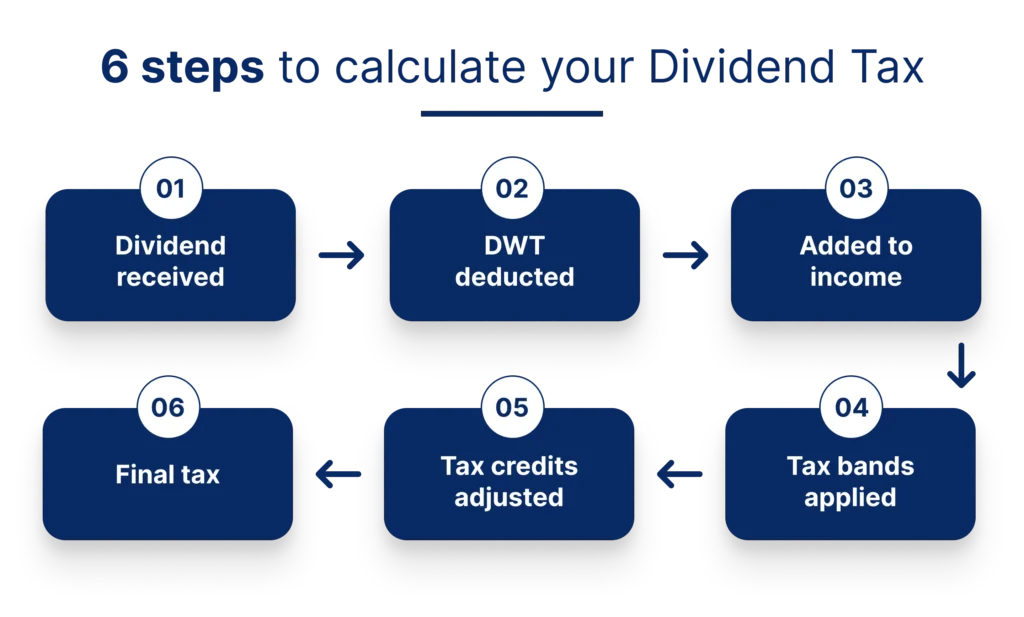

Step-by-Step: How to Calculate Tax on Dividends (Dividend Tax Calculator Ireland Method)

Follow these eight steps in order to calculate your correct liability for the 2026–27 tax year, this is effectively how any dividend tax calculator Ireland tool works behind the scenes.

Step 1: Identify your gross dividend: Your gross dividend is the full amount before DWT is deducted. If you received €15,000 in your account, the gross dividend is €20,000 and €5,000 was withheld as DWT. Always use the gross figure, not the amount that reached your account.

Step 2: Understand how DWT is deducted: The company paying the dividend withholds DWT at 25% before the payment reaches you. This is not a separate tax it is taken at source and credited against your final liability when you file your return.

Step 3: Add the gross dividend to your total income: Add the gross dividend to your salary or any other income for that year. If your other income has already used your standard rate band, the entire dividend is taxed at 40%.

Step 4: Apply the tax bands: Calculate Income Tax at 20% on any portion within your standard rate band and at 40% on any amount above it. Apply USC based on your total income for the year.

Proprietary directors and self-employed individuals with total income above €5,000 pay PRSI at 4.2% on dividends received between January and September 2026 and at 4.35% from October 2026 onwards. PAYE employees are generally not liable to PRSI on dividend income.

Step 5: Deduct DWT and adjust your tax credits: Add your Income Tax, USC and PRSI figures together to get your total liability. Then subtract the DWT already withheld at source what remains is either a balance payable or a refund due.

Step 6: Confirm your final tax position and file: Report the gross dividend on your return and enter DWT as a credit. Use Form 12 on myAccount if you are a PAYE employee with non-PAYE income under €5,000. Use Form 11 on ROS if you are a proprietary director or your non-PAYE income exceeds €5,000.

Dividend Tax Calculator Ireland

Rather than a fixed calculator, use this three-line formula to estimate your dividend tax Ireland liability before filing:

Gross Dividend × (Income Tax rate + USC rate + PRSI rate, where applicable) − DWT already withheld = Balance due or refund

For a rough dividend tax calculator Ireland estimate:

Standard-rate taxpayer (20% band): expect a refund, since 25% DWT usually exceeds your actual liability

Higher-rate taxpayer (40% band): expect a balance due, since your true liability can reach 48–49% once USC and PRSI are added

For an exact figure, work through the eight steps below or use Revenue’s myAccount/ROS system, which calculates your final liability automatically once your return is submitted.

Dividend Tax calculation: Practical examples

Example 1: Higher-rate taxpayer (Proprietary Director)

A married proprietary director draws a salary of €55,000 and declares a dividend of €24,000 from retained company profits in March 2026.

DWT deducted at source: €24,000 × 25% = €6,000. The director receives €18,000.

Total income: €55,000 + €24,000 = €79,000

The salary fills the married one-income standard rate band (€53,000 at 20%, €2,000 at 40%). The full €24,000 dividend falls above the band and is charged at 40%.

| Tax Component | Calculation | Amount |

|---|---|---|

| Income Tax at 40% | €24,000 × 40% | €9,600 |

| USC (portion at 3% and 8%) | €15,044 at 3% = €451; €8,956 above €70,044 at 8% = €716 | €1,167 |

| PRSI at 4.2% (Jan–Sep 2026) | €24,000 × 4.2% | €1,008 |

| Total tax on the dividend | €11,775 | |

| Less: DWT already paid | −€6,000 | |

| Balance due on Form 11 | €5,775 |

Effective rate: €11,775 ÷ €24,000 ≈ 49%

The 25% DWT covered just over half the actual liability. The €5,775 balance is due at filing and should be set aside in advance.

Planning note: If the dividend is paid after 1 October 2026, the PRSI rate increases to 4.35%, adding €36 to the overall tax bill. Declaring the dividend before October may reduce the PRSI liability.

Example 2: Standard-rate taxpayer (PAYE Employee)

A single PAYE employee earns €38,000 and receives a gross dividend of €1,800. Their remaining standard rate band means the dividend is taxed at 20%.

| Tax Component | Calculation | Amount |

|---|---|---|

| Income Tax at 20% | €1,800 × 20% | €360 |

| USC at 3% | €1,800 × 3% | €54 |

| PRSI | Not applicable (Class A employee) | €0 |

| Total tax on the dividend | €414 | |

| Less: DWT already paid | €1,800 × 25% | −€450 |

| Refund due from Revenue | €36 |

In this case, the company deducted more DWT than the employee was actually liable to pay. Once the tax return is filed, Revenue refunds the excess amount.

Which Dividends are Taxable in Ireland?

Not all dividends are treated the same way for Irish tax purposes. The source of the dividend determines whether DWT applies and how relief for foreign tax is calculated.

| Dividend Type | Irish DWT | Taxable in Ireland | Notes |

|---|---|---|---|

| Irish company shares | Yes, at 25% | Yes, at marginal rate | DWT credited on filing |

| Foreign dividends (general) | No | Yes, as Case III income | Foreign tax may be credited under a DTA |

| UK dividends | No | Yes, on net amount received | UK applies no withholding tax on dividends |

| US dividends | No Irish DWT | Yes, on gross amount | US withholds 30%; reduced to 15% with a W-8BEN form; Irish tax credits the US tax paid |

| Scrip dividends | Yes, at 25% | Yes, treated as cash | Additional shares valued at cash equivalent |

How does Revenue know about your Dividends?

Revenue does not rely on self-declaration alone. Irish companies and financial institutions report dividend data directly and that information reaches Revenue before you file.

Every Irish company that pays a dividend must submit a DWT return to Revenue by the 14th of the following month, listing each recipient, the amount paid and the DWT withheld. Irish stockbrokers and financial institutions send dividend data to Revenue directly as well.

For foreign income, Ireland participates in the Common Reporting Standard (CRS) and FATCA, through which foreign brokers share information on Irish-resident investors with Revenue. Dividend income that goes unreported leaves a clear paper trail and Revenue’s matching systems are designed to identify gaps.

Salary or Dividends: Which is more tax-efficient in 2026-27?

For most owner-managed directors, this decision depends on the order in which tax is applied and what each method costs at the company and personal level.

Salary is paid before Corporation Tax, so it reduces the company’s taxable profit. It also counts as pensionable earnings and builds your PRSI record.

Dividends are paid from profits that have already been subject to 12.5% Corporation Tax. They do not qualify for pension contribution relief and proprietary directors must also pay Class S PRSI, along with Income Tax and USC.

A director paying 12.5% Corporation Tax on profits and then drawing those after-tax profits as a dividend, with up to 49% personal tax applied on top, faces a combined charge that can exceed 55% on that income.

For most owner-managed directors, drawing a salary up to the standard rate band is the more efficient structure. Dividends work well as a supplement where retained profits allow, but the right mix depends on your total income, pension contribution strategy and PRSI class. Reviewing this with your accountant each year avoids unnecessary overpayment.

When to file your Dividend Tax Return for 2026-27?

The 2026-27 tax year runs from 1 January 2026 to 31 December 2026. Returns for this period are filed in 2027. The deadlines are:

| Filing Method | Deadline |

|---|---|

| Form 11 by paper | 31 October 2027 |

| Form 11 via ROS (online) | Mid-November 2027 (exact date subject to Revenue confirmation) |

| Form 12 via myAccount | Standard PAYE review cycle |

Revenue pre-fills some dividend data for PAYE users on myAccount. Always verify the figures against your dividend vouchers or broker statements before submitting.

Conclusion

Dividend tax is calculated across Income Tax, USC and PRSI at your personal rate, with the 25% DWT already deducted offset against your final liability. For 2026-27, the only change under Budget 2026 is PRSI rising from 1 October, which brings the maximum combined rate to 52.35%.

If you are a director planning a dividend for later in 2026, declaring it before October avoids the higher PRSI rate.

Outbooks supports accounting practices across Ireland with outsourcing bookkeeping, payroll and year-end accounts. To get in touch, call +353-21-206-9255 or send an email to info@outbooks.com.

Frequently Asked Questions

What is the dividend withholding tax rate in Ireland for 2026?

The Ireland dividend withholding tax rate is 25% for 2026. This is deducted at source by the paying company and treated as a credit against your final Income Tax, USC and PRSI liability.

What happens if the DWT deducted is more than my actual tax liability?

If the 25% DWT withheld is higher than what you actually owe once Income Tax, USC and PRSI are calculated, Revenue refunds the difference after you file your return. This is common for standard-rate taxpayers.

Do I need to declare dividends if DWT was already deducted?

Yes. DWT is a withholding, not a final tax. You must still declare the gross dividend on Form 11 or Form 12 and claim the DWT already paid as a credit, even if no further tax is due.

Can I offset dividend income against losses or expenses?

Dividend income generally can’t be reduced by personal expenses, but capital losses from share disposals can offset capital gains separately under CGT rules, this is a different tax from dividend tax and calculated independently.

When is the earliest a dividend can be paid from a limited company?

A company can declare a dividend as soon as it has distributable reserves, realised profits after Corporation Tax, minus prior losses. There’s no fixed waiting period, but directors should confirm reserves are legally distributable before declaring.

What is the maximum combined tax rate on dividends in Ireland for 2026–27?

For a proprietary director in the higher rate band, the combined Income Tax (40%), USC (up to 8%) and PRSI (4.35% from October 2026) can bring the effective rate close to 52%.

Are dividends from ETFs taxed the same way as company dividends?

No. Most ETFs fall under Ireland’s “gross roll-up” regime and are taxed under exit tax rules at 41%, not standard dividend tax rates, this is a key difference investors often miss.

How do I claim back dividend tax if I am a non-resident?

Non-residents can reclaim excess DWT by filing a non-resident tax return with Revenue and providing proof of residency, often via a certificate of residence from their home tax authority, especially where a double taxation agreement applies.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.