In today’s competitive landscape, businesses in Ireland must evolve beyond mere growth to achieve sustainable success. Scaling a business involves increasing revenue while improving profit margins, a concept that is particularly relevant for accountancy practices. This article explores the strategies for scaling your business through flexible accounting solutions, emphasizing the importance of technology, mindset shifts, and operational efficiency. Partnering with Outsourced Accountants can further strengthen these strategies by bringing in external expertise and cost efficiency.

What’s the difference between growing and scaling?

Growing Your Practice

If you’re merely growing your accountancy practice, you’re likely adding resources like staff, offices, and equipment. This typically results in a larger business and increased revenues. However, these new resources also lead to higher costs, which can squeeze your margins. You might take on a few more clients, increasing revenue, but if costs rise too, profits may remain stagnant or even decline.

Scaling Your Practice

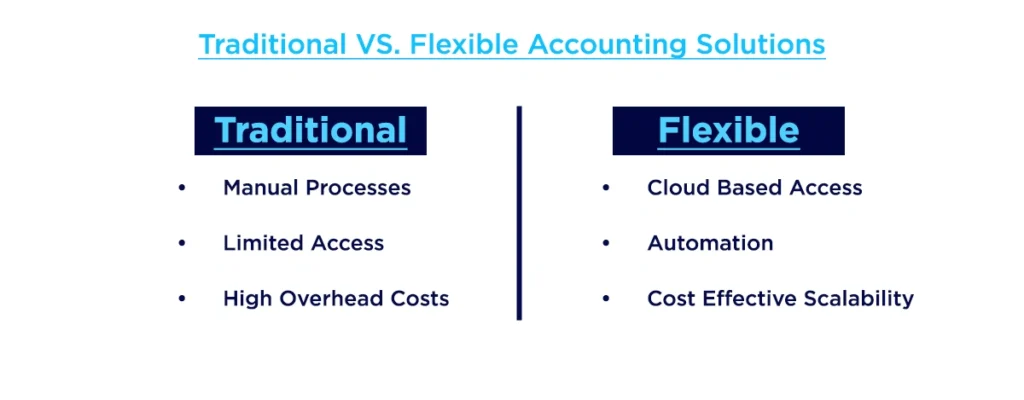

Scaling means increasing revenues while improving profit margins. Successful practices scale after their initial growth phase. Remember, growth alone doesn’t guarantee greater profits or job satisfaction. In today’s challenging economic climate, ensuring your practice is both strong and profitable is crucial. Leveraging outsourced accounting services can help firms maintain scalability by streamlining operations, reducing overheads, and enhancing financial accuracy.

As of March 2023, there were approximately 79,235 registered businesses in Northern Ireland, reflecting a 0.4% increase from the previous year. This marks the ninth consecutive year of growth following a decline from 2008 to 2014. The majority of these businesses are micro-enterprises, with 89% employing fewer than 10 people. The service sector remains the largest, accounting for 55% of all businesses and experiencing a slight growth of 0.3%. Effective scaling in this environment requires constant evaluation of business strategies to ensure sustained revenue and profitability, particularly as companies navigate challenges and opportunities in a competitive market.

Challenges involved in scaling your practice

Scaling presents various challenges, especially if it hasn’t been a focus before. A significant hurdle is a lack of information about which services are most profitable and which clients yield the best margins. Without this insight, it’s hard to know where to concentrate your scaling efforts. Other challenges include:

- Scaling faster than you’re prepared for

- Prioritizing short-term goals over long-term objectives

- Failing to optimize systems for scalability

To overcome these challenges, develop a scaling mindset that focuses on long-term growth rather than just immediate gains.

How to scale your accountancy practice

Once you understand the difference between growth and scaling, you can implement strategies to scale effectively:

- Decide on Your Scaling Goals: Define what you want to achieve and set timelines for scaling. Consider whether you want to take on more clients using technology or expand service offerings.

- Develop a Scaling Mindset: Shift your focus from merely acquiring clients to analyzing profitability. Assess whether large clients provide a good return on investment.

- Reduce Costs and Boost Profits: Look for ways to automate processes and provide bundled services without significantly increasing costs.

- Offer New Services: Retaining existing clients is cheaper than acquiring new ones. Consider offering additional services like business advice or financial planning to increase revenue from current clients.

- Develop Your Team: Invest in training your employees to enhance their skills and reduce recruitment costs. Encourage word-of-mouth referrals through incentives for existing clients.

- Delegate More: As you scale, allow employees more autonomy in decision-making while establishing clear reporting lines to avoid a blame culture.

- Create Standard Operating Processes: Document key processes for consistency across your practice, which will help with onboarding and efficiency as you grow.

- Use External Expertise When Needed: Collaborate with specialists in areas like tax planning or business consultancy to expand your service offerings without significant costs.

- Automate Processes: Implement technology solutions to automate tasks such as payroll or client onboarding, allowing your team to focus on value-added activities.

- Stay on Top of the Numbers: Use accounting software to monitor key performance indicators (KPIs) and maintain an accurate view of your practice’s financial health.

Final thoughts on flexible accounting solutions

Successful scaling requires a change in mindset along with a comprehensive review of your accounting practice. According to McKinsey, over 60% of scaling efforts can succeed when approached thoughtfully. If you’re ready to evolve your accountancy practice by focusing on scaling rather than just growing, you’ll not only benefit yourself but also your team and clients as you take this exciting step forward.

Get expert accounting and bookkeeping support tailored to your business growth at Outbooks Ireland, email info@outbooks.com or call +353-212069255 today.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.