What is financial audit

A financial audit is the review of a company’s financial statements to make sure that the financial records are fair and accurate. Financial audit is done by the professional accountants. It can be done by internal and external team both. Employees of the organization can conduct this audit. Or, it can be done externally by an outside certified public accountant (CPA) firm.

Small businesses must perform regular financial audits in order to ascertain the financial health of the company. From the point of view of the audit department, it is to analyze that if the business has correctly reported their taxable income or not.

Mainly there are two types of audits; internal and external.

Internal audits:

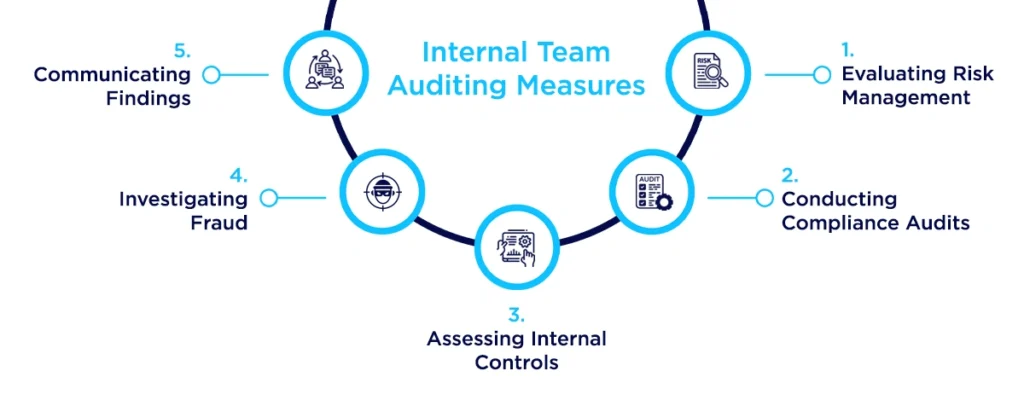

Internal audits are conducted by the company’s internal staff or the internal auditing team. This team is specifically aimed at improved operational efficiency, internal controls, and ensuring that all regulations are met with the internal policies. The team assesses risk management process, check if the company is following the internal policies, and more. Also, they examine documents, interview staff, and observe operations to identify any areas of non-compliance or inefficiencies.

There is a multi-step process that an internal auditing team goes through while conducting auditing. Once the internal team is done with the auditing part, they prepare detailed reports outlining their findings, recommendations for improvement, and any necessary follow-up actions. They present these reports to senior management and the audit committee.

The internal audit team monitors the implementation of their recommendations to ensure that corrective actions are taken effectively.

External audits:

The second type of audit is an external audit. An external audit is a kind of auditing where an external, check and scan all the financial data of the company. They will assess all the input errors and data manipulation in the financial records. Inspector collect all the evidence whether the company has attached or not.

The opinion and reports presented by these independent auditors helps the stakeholders to make an informed decision. Here is why these stake holders, trust the reports or decisions presented by these auditors.

- External auditors are independent third parties. This independence ensures an unbiased evaluation of financial information and reducing conflicts of interest.

- Auditors in Ireland are governed by stringent professional standards set by bodies like the Irish Auditing and Accounting Supervisory Authority (IAASA). These standards promote high-quality audits and enhance public trust in financial reporting.

- The audit process in Ireland is subject to oversight from regulatory authorities such as IAASA and the Financial Reporting Council (FRC). These organizations ensure that auditors adhere to established guidelines and maintain accountability.

- The presence of external auditors adds a layer of accountability for management.

- Audited financial statements carry more credibility with investors, lenders, and other stakeholders because they have been reviewed by independent experts.

Now, let us move ahead and discover why regular financial audits are important

Why regular financial audits are important for small businesses?

Regular financial audits are very important for small businesses, especially considering recent changes in the auditing field. For example, CPA Ireland has found that the number of licensed audit firms in Ireland has dropped by 31% since 2014, going from 1,542 to 1,059. This decline highlights how crucial regular audits are for making sure financial records are accurate and that businesses comply with laws, especially as there are fewer auditors available.

Additionally, the total number of auditors has decreased from 1,956 in 2018 to 1,725 last year. This means there are fewer people available to conduct audits. CPA Ireland’s President, Mark Gargan, has warned that audit costs could potentially double or even more in the next few years. Because of this, small businesses should focus on regular audits to build trust with investors and lenders.

Regular financial audits help businesses find and fix problems in their financial processes and provide reliable information needed for making smart decisions. As the auditing environment becomes more challenging due to fewer auditors and stricter regulations, having regular audits will be essential for small businesses to stay stable and grow in the long run.

As you might know that there is a threshold that you need to meet in order to come under the category of small company. These thresholds have been increased since July 1, 2024.

The new rules will start for financial years that begin on or after January 1, 2024. However, companies have the option to use the updated thresholds for financial years that start on or after January 1, 2023.

| Size – company | Original thresholds | New thresholds |

|---|---|---|

| Small company | Balance sheet total: €6 million Turnover: €12 million Employees: 50 | Balance sheet total: €7.5 million Turnover: €15 million Employees: 50 |

Audit Checklist for Small Businesses in Ireland

For small businesses in Ireland, preparing for an audit involves understanding the legal requirements and ensuring compliance with financial regulations. Below is a comprehensive audit checklist tailored to meet the needs of small businesses, focusing on documentation, internal controls, and compliance with the Companies Act 2014.

1. Understand Audit Exemption Criteria

Small companies may qualify for an audit exemption if they meet at least two of the following conditions for the current and previous financial years:

- Balance Sheet Total: Does not exceed €6 million.

- Turnover: Does not exceed €12 million.

- Number of Employees: Does not exceed 50.

If a company does not meet these criteria, it must undergo a full audit

2. Documentation Preparation

Compile essential documents to ensure readiness for an audit:

Financial Statements:

- Balance sheets

- Income statements

- Cash flow statements

- Accounts payable/receivable records

Tax Documentation:

Corporate Records:

- Articles of association

- Board meeting minutes

- Shareholder agreements.

3. Policies and Procedures

Document and review your business’s policies and procedures:

- Financial Reporting Policies: Ensure they align with current accounting standards.

- Data Privacy Policy: Comply with GDPR regulations.

- Information Security Policy: Protect sensitive information.

- Employee Conduct Policy: Establish clear expectations for employee behavior.

4. Internal Controls

Implement strong internal controls to safeguard assets and ensure accurate financial reporting:

- Segregation of Duties: Assign different people to handle different aspects of financial transactions.

- Approval Workflows: Require multiple approvals for significant expenses or changes.

- Regular Reconciliations: Perform monthly reconciliations of bank statements and accounts.

5. Data Management Practices

Establish robust data management practices:

- Data Retention Policies: Define how long documents should be kept.

- Regular Backups: Ensure data is backed up regularly to prevent loss.

- Access Control Mechanisms: Limit access to sensitive data to authorized personnel only.

6. Regular Reviews and Updates

Conduct periodic reviews of your audit readiness checklist:

- Schedule regular internal audits or mock audits to identify areas needing improvement.

- Update your policies and procedures based on feedback from audits or changes in regulations.

7. Compliance with Filing Requirements

Ensure timely filing of all necessary documents with the Companies Registration Office (CRO):

- Submit annual returns and financial statements on time to maintain eligibility for audit exemptions.

- Include any required auditor’s reports if claiming exemption

Accounting best practices for small businesses

Implementing effective accounting practices is crucial for small businesses in Ireland to ensure financial stability, compliance, and growth.

Take Ultimate Responsibility

As a business owner, it’s essential to take full responsibility for your company’s financial health. While delegation is important, regularly oversee all areas of your business. This includes understanding the basics of each function, which allows you to make informed decisions without micromanaging your staff. Trust your team but maintain a level of oversight to ensure accountability and success.

Maintain Accurate Records Continuously

Prioritize record-keeping as a fundamental part of your financial management. Keeping track of:

- Invoices: Monitor how much you are owed and by whom.

- Expenses: Document all business expenses to claim against your tax bill.

- Cash Flow: Track loans, sales revenue, and other cash inflows meticulously.

Regularly updating these records will provide a clear picture of your financial situation and help avoid penalties related to underreporting income or overestimating expenses.

Utilize Accounting Software

Invest in user-friendly cloud accounting software that simplifies your financial management. Options like Xero, QuickBooks, and Surf Accounts are popular choices among Irish small businesses. These platforms offer features such as:

- Automated invoicing

- Real-time bank reconciliation

- Multi-currency support

Using such software can save time and reduce errors, allowing you to focus on strategic aspects of your business.

Monitor Labour Costs

Hiring the right staff is vital for growth, but it’s crucial to manage labour costs effectively. Evaluate when to hire based on workload and business needs rather than impulse. Ensure that salaries are competitive but also reflect the value added by employees. This balance will help maintain profitability while fostering a productive work environment.

Create Financial Projections

Develop realistic financial projections to guide your business strategy over the next few years. Use tools like common size analysis or profit and loss statements to estimate future revenue and expenses. Collaborating with an accountant or utilizing accounting software can enhance the accuracy of these projections, helping you make informed investment decisions and identify potential funding needs. This was all about “Importance Of Regular Financial Audits For Small Business”.

Contact us today via call +353 212069255 or mail at info@outbooks.com.

FAQs

What does regular audits mean?

Regular audits mean checking financial records and processes regularly to ensure accuracy and compliance.

What are the 3 main types of audits?

There are various types of audits, some of the most common ones include, external audit, tax audit, internal audit, compliance audit and statutory audit.

What do you mean by financial audit?

A financial audit is a review of a company’s financial records to ensure they are accurate and follow laws and regulations.

What is the process of financial audit?

The process of a financial audit involves, Planning, Fieldwork, Testing and Reporting

Who does a financial audit?

A financial audit is typically performed by auditors, who are usually accountants or CPAs.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.