R&D tax credits in Ireland give businesses a way to recover cost spent on research and development. Following Budget 2026, the credit rate has risen to 35% and cash refunds for smaller and loss-making businesses have become more accessible.

Most Irish businesses that qualify do not claim the full amount available to them. Product development, process improvements and software projects can all qualify, but many businesses do not realise how much of their activity is eligible.

This guide covers who qualifies, what cost can be claimed and how to make a successful R&D tax credit claim in Ireland in 2026.

Key Takeaways

- Budget 2026 increased the Irish R&D tax credit rate from 30% to 35% for Irish businesses and they can now claim 35% of qualifying R&D expenditure.

- The first-year payment threshold increased from €75,000 to €87,500, allowing smaller Irish companies to access a larger cash refund in the first year of their claim.

- Irish companies that are loss-making or in a pre-profit stage can still claim the R&D tax credit as a cash refund from Revenue, paid in annual instalments over three years.

- Qualifying R&D expenditure includes staff cost, consumables, software and subcontractor cost the activity must meet Revenue’s definition of systematic research aimed at resolving scientific or technological uncertainty.

What are R&D Tax Credits in Ireland?

The research and development tax credits in Ireland allow businesses to claim back part of what they spend on improving a product, process or software where there is no clear solution at the start.

This usually involves fixing issues, improving performance or testing different approaches to make something work.

From 2026, the credit is 35% of eligible R&D cost. So, if a business spends €100,000 on qualifying work, it may be able to claim back €35,000.

The credit is used to reduce corporation tax and if there is no tax to pay, the balance can be received as cash over time.

Who Qualifies for R&D Tax Credits in Ireland?

Any company subject to Irish corporation tax that carries out qualifying R&D in Ireland, the EU or the EEA can claim. There is no minimum size SMEs, startups and larger firms all qualify.

To be eligible, the activity must:

- Follow a systematic and investigative approach

- Aim to achieve a scientific or technological advancement

- Involve resolving uncertainty that cannot be easily solved using existing knowledge

The work does not need to produce a successful outcome as long as a genuine attempt at investigation was made, it can still qualify.

Common sectors in Ireland include software development, pharmaceutical and biotech research, medical device development, manufacturing process innovation and other R&D developments.

Already qualify? Let Outbooks handle your Corporation Tax Return so your R&D credit claim is filed accurately and on time.

What Does Not Qualify as R&D?

Not all development work qualifies for R&D tax credits. Some common examples of non-qualifying activities include:

- Routine software updates, bug fixes or maintenance work

- Work that follows an already established method or known solution

- Cosmetic or design-only changes that do not involve technical uncertainty

- Data migration or system upgrades without any experimentation

Understanding this distinction is important, as many claims are reduced when non-qualifying work is included.

What Qualifying R&D Expenditure Can Be Claimed?

Qualifying expenditure falls into clear categories:

| Expenditure Category | What Qualifies | Key Condition |

|---|---|---|

| Employee cost | Salaries, wages, employer PRSI for staff working on R&D | If 95%+ of their time is on qualifying R&D, 100% of salary qualifies (Budget 2026 rule) |

| Consumables | Materials, reagents, lab supplies used in R&D | Must be used directly in the R&D work |

| Software | Software used primarily in development counts as R&D tax credit software if integral to the process. | Must be integral to the R&D process |

| Subcontractor cost | Third parties carrying out R&D on your behalf | Subject to limits: 15% of R&D spend or €100,000, whichever is greater |

| Plant and machinery | Depreciation on equipment used for R&D | Proportionate to R&D use |

The Budget 2026 employee cost rule is a meaningful change. Previously, Revenue required detailed time apportionment for employees partly engaged in R&D.

Under the new rule, if at least 95% of an employee’s time is spent on qualifying R&D, 100% of their salary qualifies reducing the administrative burden for businesses with dedicated R&D staff.

How to Make an R&D Tax Credit Claim in Ireland?

Claiming the R&D tax credit works best when approached step by step. Keeping records organised ensures the claim is correct and can be supported if Revenue asks for details.

For example, a software company testing a new algorithm can track staff hours, materials and software cost throughout development, making the claim easier to prepare.

Step-1 Identify Qualifying Projects

Start by reviewing your projects to see which involve genuine scientific or technological uncertainty. Qualifying projects are those that:

- Try to solve a problem that cannot be answered using existing knowledge

- Involve testing, experimentation or systematic investigation

- May not always succeed but are genuinely innovative

Document the goals, challenges and methods used in each project. Written notes kept during the project are essential for Revenue verification.

Step-2 Gather Qualifying Cost

Collect all cost directly related to qualifying R&D:

- Employee cost: Salaries, wages and employer PRSI for staff mainly working on R&D.

- Consumables: Materials or lab supplies used directly in the project.

- Software: Programs essential to the R&D process.

- Subcontractors: Third-party R&D work up to 15% of total R&D spend or €100,000, whichever is greater.

For example, a biotech company developing a new assay can include lab reagents, specialised software and subcontracted testing cost. Keep invoices, payroll records and contracts as evidence to support tax credit claims.

Step-3 Calculate the Credit

Calculate the research and development tax credit by adding qualifying cost and multiplying by 35%. This is the amount your company can claim. Clear categorisation and supporting records make the claim easier to check and defend if Revenue reviews it.

Step-4 File Through Corporation Tax Return

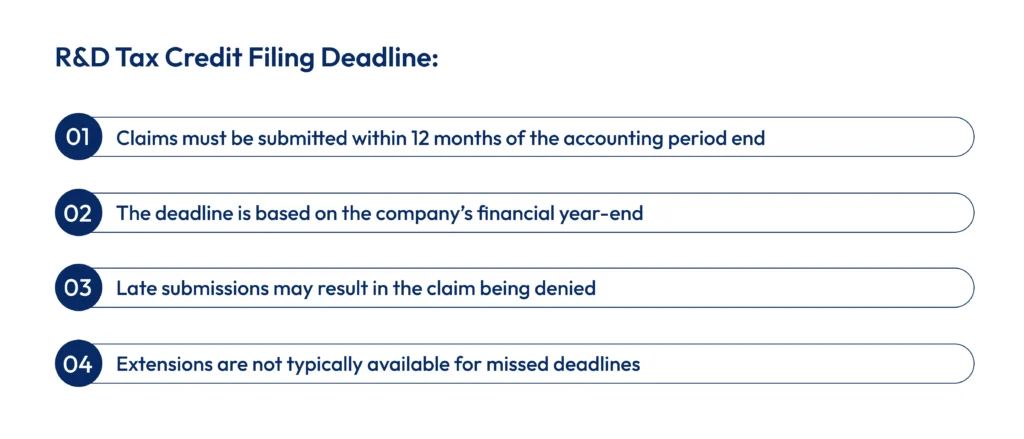

Submit your R&D tax credit claim using Form CT1 within 12 months of the accounting period end. This 12‑month filing deadline is strict, missing it can result in a claim being denied, even if all work and cost were legitimate.

Ensure the claim references each project and associated cost and that documentation is organised and easy to follow.

Step-5 Receive Payment

Offset the credit against any corporation tax liability. Excess amounts are refunded as a cash payment from Revenue, paid in three equal annual instalments up to the first-year threshold of €87,500.

Organising project notes and financial records throughout the year ensures the claim process is simple and reduces the chance of Revenue queries.

Note: First-time claimants (or those who haven’t claimed in the past three years) must also submit a Pre-Filing Notification to Revenue at least 90 days before filing.

Keeping Proper Records for an R&D Tax Credit Claim

Revenue can ask to review your claim at any point. When it does, it will want to see what your team worked on, how much time they spent and what made the work uncertain. Keeping records as the project runs is what protects your claim.

What to include:

- Project Details: A description of each project and the uncertainty or challenge it aimed to solve.

- Staff Involvement: Time spent by team members on R&D activities, ideally recorded per project.

- Supporting Documents: Invoices, payroll records, purchase orders and contracts for any subcontracted work.

Most claims that get reduced come down to the same issues: records put together at the last minute, no time logs for staff cost or project descriptions that do not explain what made the work uncertain.

Need accurate payroll records for your R&D claim? Outbooks Payroll Services keeps your staff cost documented and compliant.

Can Startups and Loss-Making Companies Claim R&D Tax Credits?

This is one of the most common misconceptions around Irish R&D tax credits and it stops many early-stage companies from claiming money they are entitled to.

A company does not need to be profitable to claim. For loss-making companies, the credit that cannot be offset against corporation tax is refunded as a cash payment from Revenue, paid in three equal annual instalments over three years.

Budget 2026’s increase in the first-year threshold to €87,500 is particularly valuable for early-stage companies, as it means smaller claims are paid in full in year one. There is no minimum trading period required, companies can claim from their first year of qualifying R&D expenditure.

R&D Tax Credit vs R&D Grant: What is the Difference?

Many Irish businesses assume an R&D tax credit and an R&D grant work the same way. They do not. One is a right you can claim if you qualify. The other is a competition you have to enter and may not win.

- R&D Tax Credit: Any Irish company that meets Revenue’s criteria can claim back 35% of qualifying R&D expenditure through their corporation tax return. There is no application process and no competition involved.

- R&D Grant: Funding awarded by bodies like Enterprise Ireland or IDA Ireland that you have to apply for. It is tied to specific projects and outcomes and there is no guarantee you will receive it.

The most important rule when using both is this: if a grant has already covered part of your R&D cost, you cannot claim the research and development tax credit on that same expenditure.

Both incentives can be used on the same project, but the same spend cannot be counted twice when claiming R&D tax relief.

Common Mistakes to Avoid When Claiming R&D Tax Credits

Even when the work qualifies, claims can still be reduced or rejected. In most cases, it comes down to a few common mistakes.

- Late or Missing Records: Some businesses only gather documents when they are ready to file the claim. Revenue expects records that were kept during the project, not created later from memory.

- Unclear Project Explanation: It is not enough to say what was built. You need to explain what problem you were trying to solve, what made it difficult and why the answer was not already known.

- No Record of Staff Time: If you are claiming employee cost, you need to show how much time was spent on R&D work. Without proper time records, that part of the claim may be reduced.

- Including Non-Qualifying Work: Regular updates, maintenance, or work that follows a known method should not be included. Adding these can weaken the claim and lead to questions.

Getting these basics right from the start makes the claim easier and reduces the chances of Revenue raising queries.

Conclusion

Budget 2026 increased the Irish R&D tax credit to 35%, raised the first-year payment threshold to €87,500 and allows loss-making companies to get a cash refund, making it a good time to claim.

To get the most from your R&D tax credit, businesses should identify qualifying projects early, keep clear records throughout the year and file the claim within 12 months of the accounting period end. Clear financial documentation and organised cost, payroll and project records help make the process straightforward and supportable.

Outbooks supports Irish businesses through outsource accounting and bookkeeping services, ensuring cost records, payroll allocations and financial documents are clear, complete and ready whenever needed. To learn more, call +353-21-2069255 or email info@outbooks.com.

FAQs

What is the R&D tax credit rate in Ireland for 2026?

The R&D tax credit rate in Ireland for 2026 is 35% of qualifying R&D expenditure for eligible companies.

Who qualifies for R&D tax credits in Ireland?

Any Irish company paying corporation tax, including SMEs, startups and larger businesses, carrying out eligible R&D in Ireland, the EU or EEA can claim R&D tax credits.

What expenses can be included in an R&D tax credit claim in Ireland?

Qualifying R&D expenditure includes employee salaries, employer PRSI, consumables, software, subcontractor cost and plant or machinery used directly for R&D.

How long does Revenue Ireland take to process an R&D tax credit claim?

Revenue Ireland does not specify a standard timeline for R&D tax credit claims; the claim is submitted within your Corporation Tax Return (CT1) via ROS and processing varies according to claim complexity and documentation quality repayments occur in up to three annual instalments.

What is the deadline for filing an R&D tax credit claim in Ireland?

R&D tax credit claims must be submitted within 12 months of the end of the accounting period in which the R&D expenditure was incurred, via the Corporation Tax return (Form CT1).

What is the difference between an R&D tax credit and an R&D grant in Ireland?

R&D tax credits reduce corporation tax or provide a cash refund, while R&D grants give upfront funding for specific research or development projects.

Do I need an R&D tax credit consultant to make a claim in Ireland?

Consultants are not required, but they help ensure R&D credit claims are accurate, fully documented and compliant with Revenue Ireland rules.

What to look for when hiring tax relief consultants in Ireland?

Choose consultants experienced in Irish R&D tax credits, familiar with qualifying activities and capable of maintaining clear project and cost records.

How do I claim R&D tax credits in Ireland?

Identify eligible projects, track qualifying cost, calculate your R&D credit and submit the claim via Form CT1 with your corporation tax return.

Can I claim R&D tax credits for previous years in Ireland?

Yes, you can claim Ireland’s R&D tax credits for the previous accounting period if within the 12-month deadline from its end, but not generally for multiple prior years beyond that.

Are there any changes to the R&D tax credit scheme in Ireland for 2026?

Yes, the credit rate increased to 35%, the first-year payment threshold rose to €87,500 and cash refunds are available for loss-making companies.

How can managing accounting and R&D records help with claiming the credit?

Organising cost records, payroll and purchase documentation ensures R&D tax credit claims in Ireland are accurate, easy to support and compliant with Revenue requirements.

What are common mistakes businesses make when claiming R&D tax credits?

Frequent errors include incomplete documentation, vague descriptions of R&D work, claiming non-qualifying activities and misallocating employee cost, which can reduce or reject claims.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.