Choosing between a sole trader or limited company is one of the major decisions a business owner makes in Ireland. The structure affects how profits are taxed, the level of personal liability involved, the administrative obligations required and the options available when the business is eventually sold or transferred.

While a limited company can offer tax advantages in certain circumstances, it is not automatically the better option. For many smaller businesses, the additional compliance cost may not justify the potential tax savings.

This guide explains how sole traders and limited companies are taxed in 2026, where the potential tax advantages exist and how to determine which structure is likely to suit your situation.

Key takeaways

- Sole traders pay income tax on all profit the combined marginal rate exceeds 52% above €70,044

- A limited company pays 12.5% corporation tax on profit retained inside the business

- Below €40,000 to €50,000 in net profit, the compliance cost of a limited company usually cancels the tax saving

- Pension contributions are significantly more tax-efficient through a limited company

- From January 2026, the Revised Entrepreneur Relief lifetime limit increased to €1,500,000

Difference between a Sole Trader and a Limited Company in Ireland

The legal difference between the two structures determines everything tax, personal risk and what happens to the business long term.

A sole trader and their business are the same legal entity. Every euro of profit is personal income. Every debt or claim against the business is a claim against you personally.

A limited company is a separate legal entity. It earns its own income, holds its own liabilities and files its own tax returns. Directors are taxed separately on salary, benefits or dividends received from the company.

| Factor | Sole Trader | Limited Company |

|---|---|---|

| Legal status | Same as owner | Separate legal entity |

| Personal liability | Unlimited | Limited to share capital |

| Tax on profit | Personal income tax rates | 12.5% corporation tax |

| Accounts filed publicly | No | Yes, with CRO |

| Business continuity | Ends with owner | Continues independently |

The legal structure also determines who is responsible when the business owes money, faces a claim or encounters financial difficulty.

How is each Structure Taxed in 2026?

The tax rates are where the real difference between the two structures becomes visible and the gap is larger than most people expect before they look at the numbers.

Sole trader tax structure

All business profit is personal income. Revenue charges it in the year it arises whether you draw it or not. There is no way to reduce this by leaving money in the business.

| Tax | 2026 Rate |

|---|---|

| Income tax standard rate | 20% on first €44,000 |

| Income tax higher rate | 40% above €44,000 |

| USC | 0.5% to 8% tiered |

| USC surcharge self-employed | Extra 3% above €100,000 |

| PRSI Class S | 4.2% Jan–Sep, 4.35% from Oct 1 (blended rate 4.2375%) |

| Earned Income Tax Credit | €2,000 max (20% of qualifying earned income) |

Above €70,044, a sole trader pays 40% income tax, 8% USC and 4.2% PRSI on every additional euro of profit a combined marginal rate of over 52%.

Limited company tax structure

The company pays 12.5% corporation tax on active trading profits. You draw a salary taxed at personal rates through PAYE. Profit left in the company after your salary stays at 12.5% only until you take it out. Passive income such as rent or investment returns is taxed at 25%.

| Factor | Sole Trader | Limited Company |

|---|---|---|

| Retained profit | 52%+ regardless | 12.5% CT only |

| Salary drawn | Personal rates | Personal rates |

| USC on profit | All profit | Salary only |

| PRSI on profit | All profit | Salary only |

| Pension contributions | Income tax relief only | Deductible before CT, no USC or PRSI |

The tax a limited company pays depends largely on what happens to its profits. Keeping profits within the business and withdrawing them for personal use can lead to very different tax outcomes.

Which Structure Saves more Tax: Sole Trader or Limited Company

For many growing businesses, a limited company can save more tax than operating as a sole trader.

A sole trader is taxed on all business profits as personal income. A limited company pays corporation tax at 12.5% on trading profits kept in the business.

If all profits are taken out as salary, the tax difference is smaller than most people expect. If some profits stay in the company, the advantage becomes much more significant.

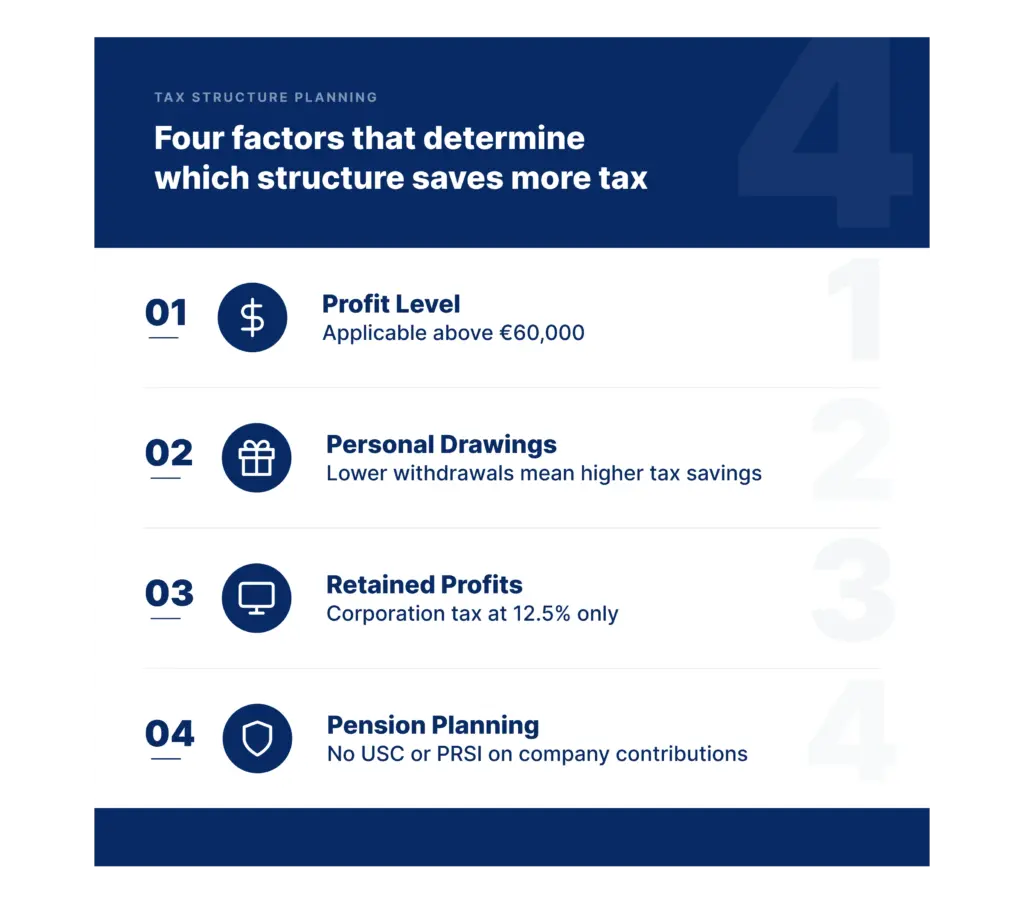

Whether a limited company saves more tax depends on four factors:

Profit level

At lower profit levels, the annual cost of running a limited company often cancels the tax saving. Once profit grows, the gap between 12.5% and the 52% combined rate a sole trader pays starts to matter.

| Annual Net Profit | Typical Position |

|---|---|

| Under €40,000 | Sole trader usually more practical |

| €40,000 to €60,000 | Depends on circumstances |

| Above €60,000 | Limited company often more attractive |

| €80,000 and above | Potentially significant tax saving |

Profit alone does not determine whether incorporation saves tax. The amount withdrawn from the business each year is often just as important.

Your personal drawings

How much money you need personally each year can be just as important as overall profit.

If all profits are withdrawn for personal use, much of the income ultimately becomes subject to personal tax rates regardless of structure.

The tax advantage of incorporation becomes stronger when not all profits are needed immediately.

Retained profits

Retained profits are often where the largest tax advantage exists.

For example, a director earning €100,000 who only requires €60,000 personally can leave €40,000 inside the company.

That retained amount is taxed at 12.5% corporation tax rather than potentially facing income tax, USC and PRSI at the higher combined marginal rate.

The difference on retained profits can be significant over time and can provide funds for future expansion, recruitment or investment.

Pension planning

A company pays employer pension contributions from trading profit before corporation tax is calculated. No income tax, USC, or PRSI applies to those contributions for the director.

A sole trader gets income tax relief on contributions but USC and PRSI still apply to the profit behind them. Tax savings are often the reason business owners start looking at incorporation in the first place.

When should one consider moving to a Limited Company?

Many businesses start as a sole trader and later transition to a limited company as profits grow.

A move from sole trader to limited company may be worth considering when:

- Annual profits consistently exceed €60,000

- Not all profits are required for personal spending

- Pension planning becomes a priority

- Staff are being employed

- Business risks are increasing

- A future business sale is being considered

Liability protection

A limited company is a separate legal entity from its owners. In most cases, business liabilities remain with the company rather than the shareholders.

By contrast, a sole trader and the business are legally the same entity. Business debts, legal claims and financial obligations remain the personal responsibility of the owner.

As a business grows, liability protection can become just as important as potential tax savings.

Registration and compliance

The administrative requirements are also different. Sole traders register with Revenue using Form TR1. For those looking to register as a sole trader in Ireland, file a Form 11 income tax return each year.

If they are trading under a business name rather than their own, they must also complete sole trader business registration with the CRO for €20. There is no annual CRO return requirement and business accounts remain private.

A limited company must be incorporated with the CRO, with an online incorporation fee of €50 , before registering with Revenue using Form TR2 .

Companies are subject to ongoing compliance obligations, including annual CRO filings and corporation tax returns. Where directors are paid through payroll, PAYE registration is also required.

| Obligation | Sole Trader | Limited Company |

|---|---|---|

| Revenue registration | TR1 via ROS | TR2 via ROS |

| CRO registration fee | €20 for business name only | €50 |

| Annual CRO return | Not required | B1 Annual Return |

| Accounts filed publicly | No | Yes |

| Annual tax return | Form 11 | Form 11 (director) + CT1 |

Future growth

A limited company may be more suitable where there are plans to employ staff, bring in investors, build long-term business value or eventually sell the business.

For many business owners, the decision to move from a sole trader to a limited company is based on a combination of tax efficiency, liability protection and future growth plans rather than any single factor alone.

The choice can also affect the reliefs available when the business is eventually sold or transferred.

Retirement and Exit Strategies

The choice between a sole trader and a limited company can also influence the retirement and exit strategies available when the business is sold or transferred.

Retirement Relief

Retirement Relief removes or reduces CGT on qualifying business disposals for owners aged 55 or over.

For third-party sales, full relief applies up to €750,000 for those aged 55 to 69 or €500,000 for those aged 70 or over. Both sole traders and limited company owners may qualify, subject to the relevant Revenue conditions.

Revised Entrepreneur Relief

Revised Entrepreneur Relief may apply where Retirement Relief does not fully eliminate the gain. From January 2026, the lifetime limit is €1,500,000, with qualifying gains taxed at 10% CGT instead of the standard 33% rate.

To qualify, the individual must have owned qualifying business assets continuously for at least three years within the five years immediately before the disposal.

Selling a limited company is also generally simpler in practice. Ownership can transfer through a share sale in a single transaction, whereas a sole trader business typically requires individual assets and contracts to be transferred separately, which buyers may factor into their valuation.

Selling a business

Selling a limited company is also simpler in practice. Ownership passes through a share sale in a single transaction.

A sole trader business requires assets and contracts to be transferred separately something buyers factor into any offer they make.

Advantages and Disadvantages of a Sole Trader vs Limited Company

Each structure comes with its own benefits and trade-offs. Understanding how they differ can help you decide which option best aligns with your business goals, tax position and long-term plans.

Sole trader

- Simple and free to register

- Lower annual accountancy cost

- Accounts stay private

- All profit taxed at personal rates regardless of what you draw

- Personal assets at risk if the business owes money

Limited company

- 12.5% tax on retained profit

- More tax-efficient pension contributions

- Personal assets protected in most situations

- Cleaner on exit and easier to sell

- Higher annual compliance cost

- Accounts filed publicly with the CRO each year

Whether incorporation makes sense depends on how those advantages compare with the additional obligations involved.

Should you stay a Sole Trader or Incorporate a Limited Company?

The right structure depends on where your business stands today and where you plan to take it.

Most business owners choose to incorporate once profits reach a level where the tax and commercial benefits justify the additional obligations.

If annual profit is below €40,000 to €50,000, operating as a sole trader is often the more practical option. At that level, the additional compliance cost of a limited company can reduce much of the potential tax saving.

Where profits consistently exceed that range, part of the profit can be retained within the business and pension planning becomes a priority, a limited company may offer meaningful tax advantages.

A limited company may also be worth considering where there are plans to bring in investors, employ staff, build long-term business value or eventually sell the business.

Most business owners choose to incorporate once profits reach a level where the tax and commercial benefits justify the additional obligations.

The structure that produces the lowest overall tax cost is not always the one with the lowest headline tax rate. The key considerations are how much profit is retained, how much is needed personally and what plans exist for the business over the long term.

Conclusion

For businesses generating lower profits and requiring most earnings for personal use, operating as a sole trader is often the simpler and more practical choice. As profits increase and some income can be retained within the business, a limited company may offer advantages through lower tax on retained profits, more efficient pension funding and greater liability protection.

The right structure is not determined by tax rates alone. Profit levels, personal income needs and long-term business plans should all be considered before making a decision.

Outbooks team works with sole traders and limited companies across Ireland on bookkeeping, VAT, year-end accounts, CT returns and payroll. Get in touch at info@outbooks.com or call +353 212069255.

FAQs

Can a sole trader register a business name in Ireland?

Yes, for €20 online with the CRO. This does not create a separate legal entity. The sole trader remains personally liable for all debts under that name.

Can I be both a sole trader and a director of a limited company?

Yes, Revenue treats them as completely separate. Sole trader income is declared on a personal Form 11. The company files its own CT1 corporation tax return.

Does a sole trader have a company registration number in Ireland?

No, sole traders do not get a company registration number. Revenue assigns a tax registration number linked to the owner’s PPS number. Only incorporated limited companies receive a CRO number.

Do sole traders pay corporation tax in Ireland?

No, corporation tax applies to limited companies only. Sole traders pay income tax, USC and PRSI Class S on business profits through the personal tax system.

Can a sole trader claim VAT back in Ireland?

Yes, once VAT registered. Input VAT on qualifying business purchases is offset against output VAT on returns filed through ROS.

How do I file income tax as a sole trader, Form 11 or Form 12?

Form 11, filed through ROS. The paper deadline is 31 October, online filers get an extension to mid-November. Form 12 is for PAYE employees only. Late filing carries a surcharge of 5% or 10%.

What exit strategies are available to sole traders in Ireland?

A sole trader can sell business assets, transfer to a family member or cease trading. Retirement Relief and Revised Entrepreneur Relief may reduce CGT on disposal. From 1 January 2026, the Revised Entrepreneur Relief lifetime limit is €1.5 million.

Is it easier to sell a limited company or a sole trader business?

Yes, generally a limited company is easier. Ownership transfers through a single share sale. Selling a sole trader business requires transferring individual assets and contracts separately, which buyers typically price as added complexity.

Can a sole trader register a business name in Ireland? Yes, for €20 online with the CRO. This does not create a separate legal entity. The sole trader remains personally liable for all debts under that name.

Can I be both a sole trader and a director of a limited company? Yes, Revenue treats them as completely separate. Sole trader income is declared on a personal Form 11. The company files its own CT1 corporation tax return.

Does a sole trader have a company registration number in Ireland? No, sole traders do not get a company registration number. Revenue assigns a tax registration number linked to the owner’s PPS number. Only incorporated limited companies receive a CRO number.

Do sole traders pay corporation tax in Ireland? No, corporation tax applies to limited companies only. Sole traders pay income tax, USC and PRSI Class S on business profits through the personal tax system.

Can a sole trader claim VAT back in Ireland? Yes, once VAT registered. Input VAT on qualifying business purchases is offset against output VAT on returns filed through ROS.

How do I file income tax as a sole trader, Form 11 or Form 12? Form 11, filed through ROS. The paper deadline is 31 October, online filers get an extension to mid-November. Form 12 is for PAYE employees only. Late filing carries a surcharge of 5% or 10%.

What exit strategies are available to sole traders in Ireland? A sole trader can sell business assets, transfer to a family member or cease trading. Retirement Relief and Revised Entrepreneur Relief may reduce CGT on disposal. From 1 January 2026, the Revised Entrepreneur Relief lifetime limit is €1.5 million.

Is it easier to sell a limited company or a sole trader business? Yes, generally a limited company is easier. Ownership transfers through a single share sale. Selling a sole trader business requires transferring individual assets and contracts separately, which buyers typically price as added complexity.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.