An Accounting Audit in Ireland is an examination of your organisation’s financial information. This examination is conducted by an independent auditor. The aim is to ensure information is represented fairly and accurately.

Auditing in accounting plays an important role in achieving transparency in business operations. It also increases investors’ confidence in the business growth. Modern audit processes help ensure financial reports are both accurate and comply with regulations.

This guide helps Irish businesses get ready for accounting audits. We’ll walk you through the audit process from start to finish, show you what paperwork you need to have ready, and explain the different types of audits. You’ll also get helpful tips to stay on top of the rules. By following this guide, you’ll make sure your financial records are correct, clear, and ready to be checked. This helps you avoid common mistakes and shows your bank, investors, and partners that they can trust you.

10 Major goals of an Accounting Audit

Below are the major accounting goals:

- Transparency: To achieve transparency in business operations and drive accountability.

- Audit Trail: To develop a practice of having an audit trail for each transaction.

- Independent Opinion: To have an independent and fair opinion on how the business works.

- Quality Assurance: To ascertain the quality of financial statements

- Process Feedback: To deliver 360 feedback on the business process operations.

- Investor Attraction: To attract new and potential investors or stakeholders.

- Compliance: To ensure compliance with tax laws and accounting standards.

- Stakeholder Assurance: To provide assurance that financial statements are reliable.

- Improvement Areas: To identify areas for improvement in financial reporting.

- Fraud Detection: To detect and prevent fraud and other financial irregularities.

Audit requirements for different company sizes in Ireland

Understanding whether your company needs an audit depends on its size. Irish company law divides businesses into categories based on specific thresholds.

Small Companies (Audit Exempt)

Your company can skip the audit requirement if it meets two of these three conditions:

- Turnover of €12 million or less

- Balance sheet total of €6 million or less

- 50 employees or fewer

However, you still need an audit if:

- Your company is part of a group that doesn’t qualify as small

- Your shareholders (holding at least 10% of shares) request an audit

- Your Articles of Association require it

Medium & Large Companies (Audit Required)

If your company exceeds two of the small company thresholds, you must have your accounts audited annually.

Public Limited Companies (PLCs)

All PLCs must have audited accounts, regardless of size.

Special Cases

Certain types of companies always need audits:

- Banks and insurance companies

- Investment firms

- Companies traded on stock markets

- Credit unions

Important Note: Even if you’re exempt from an audit, you still must file annual returns with the Companies Registration Office (CRO) and prepare proper accounts.

Internal Accounting Audit vs External Accounting Audit

| Feature | Internal Audit | External Audit |

|---|---|---|

| Conducted by | Internal auditors (company employees) | External auditors (independent professionals) |

| Focus | Internal controls, risk management & operations | Accuracy & fairness of financial statements |

| Purpose | Process improvements and risk identification | Opinion on financial statement compliance |

| Requirement | Not mandatory, discretionary | Mandatory for public companies |

| Outcome | Management guidance for efficiency | Credibility for stakeholders |

Step by step Accounting Audit Process

The external accounting audit process follows these common steps globally. These steps are also applicable for audit and accounting procedures in Ireland.

1. Planning and Goal-Setting

After engaging an external auditor, your organisation discusses the engagement level. You also set the process and objectives of the auditing process. A timeline is established so your organisation can prepare properly.

Key Actions:

- Define audit scope and objectives

- Set realistic timelines

- Conduct preliminary internal audit

2. Requesting Financial Information

The auditor creates a comprehensive list of required financial documents. This accounts audit checklist typically includes previous audited reports and bank statements. It also covers ledgers, receipts, and board meeting minutes.

Essential Documents for Ireland:

- Annual audited accounts

- Tax returns and correspondence

- Bank statements and reconciliations

- General ledgers and trial balances

- Board meeting minutes

- Organisational charts

3. Performing Audit and On site examination

The auditor executes planned audit procedures once all documents are received. This includes examining financial records and conducting interviews. It also involves testing internal controls and verifying transactions.

Key Activities:

- Data sampling and transaction testing

- Internal controls evaluation

- Anomaly identification

- Evidence gathering

4. Analysing findings & preparing Audit report

The auditor drafts a comprehensive report based on examination findings. This report mentions any proof of fraud or financial mismanagement. It includes

suggestions for improving internal controls.

Internal Audit preparation steps

Your accounting and auditing team can follow these steps for internal audit preparation:

Pre-Audit Preparation

Define Focus Areas:

- Clearly establish audit questions

- Identify key risk areas

- Set measurable objectives

Assemble Audit Team:

- Include necessary skills and knowledge

- Assign specific responsibilities

- Ensure adequate training

Document Collection:

- Create comprehensive document list

- Gather all required processes

- Identify review variables

During Internal Audit

Information Collection:

- Conduct employee interviews

- Perform detailed research

- Use multiple collection methods

Risk Assessment:

- Evaluate internal control systems

- Assess functional area risks

- Document control weaknesses

Evidence Analysis:

- Analyse collected evidence

- Evaluate operational impact

- Identify improvement areas

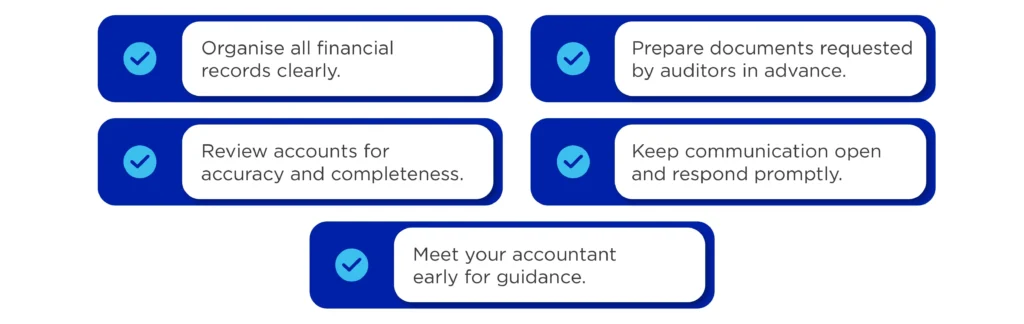

Best practices for interaction with Auditors

How you communicate with your auditors can make a big difference in how smoothly the audit goes. Here’s how to create a positive, productive relationship:

Before the Audit starts

Be Prepared:

- Have all documents organised and ready

- Review your own records first to spot potential issues

- Prepare explanations for any unusual transactions

- Make sure your staff knows the audit is happening

Set clear expectations:

- Agree on timelines and deadlines

- Establish who the main contact person will be

- Arrange for workspace if the auditor is coming on-site

- Confirm what format they want documents in (paper, PDF, direct system access)

During the Audit

Respond Quickly:

- Answer queries within 24-48 hours when possible

- If you need time to find information, give them a realistic deadline

- Don’t ignore requests hoping they’ll forget

Be Honest and Transparent:

- If you made a mistake, admit it

- Don’t hide problems or difficult transactions

Post audit compliance and documentation storage

The audit doesn’t end when the auditor leaves. Proper follow-up and storage of records are essential for ongoing compliance.

Immediate Post audit actions

Review the Audit Report Carefully:

- Read the auditor’s opinion and understand what it means

- Review any management letter highlighting weaknesses or suggestions

- Discuss unclear points with your auditor

File Your Accounts:

- Submit audited accounts to the Companies Registration Office (CRO) within 28 days of the Annual Return Date (ARD)

- Late filing results in automatic fines starting at €100 and increasing daily

- File online through CORE (Companies Online Registration Environment) for faster processing

Business expense rules for Irish Audits

Based on Revenue Commissioners guidance applicable to Irish businesses, expenses must meet the “wholly and exclusively” test. For an expense to be tax-deductible, it must be incurred wholly and exclusively for trade purposes. This principle is fundamental to audit and accountancy practices.

| Expense Type | Common Issues | Audit Focus |

|---|---|---|

| Travel & Meals | Personal lunch claims, home-to-work travel | Business purpose verification |

| Vehicle Expenses | 100% cost claims for mixed-use vehicles | Business proportion calculation |

| Home Office | Inappropriate household cost claims | Exclusive business use evidence |

| Training | Non-deductible new skill development | CPD vs new qualification distinction |

| Entertainment | Client entertainment assumptions | Non-deductible nature confirmation |

CPD is the ongoing training and education that qualified auditors and outsourced accountants must complete to maintain their professional licenses.

Calculating business expense apportionment

Your outsourced accounting and auditing services must ensure proper apportionment methods:

Requirements:

- Proper record support (mileage logs, timesheets)

- Consistent year-over-year application

- Reasonable and justifiable calculations

Documentation Needed:

- Detailed mileage records

- Time allocation sheets

- Receipt collections

- Business use calculations

Audit documentation checklist

Below is the final audit checklist you should keep handy:

Financial documents

Core Financial Records:

- Trial balance and general ledger

- Profit and loss accounts

- Balance sheet statements

- Cash flow statements

- Bank reconciliations

Supporting Documentation:

- Invoice files and receipts

- Purchase orders and contracts

- Payroll records and employment files

- Tax returns and correspondence

- Insurance policies and claims

Internal controls documentation

Process Documentation:

- Internal control procedures

- Authorisation matrices

- Segregation of duties charts

- Risk assessment documents

- Compliance monitoring records

System Documentation:

- Accounting software manuals

- User access controls

- Backup and recovery procedures

- Data security measures

- Change management processes

Compliance & risk management

Key Compliance Areas:

- International Financial Reporting Standards (IFRS)

- Generally Accepted Accounting Principles (GAAP)

- Irish company law requirements

- Tax compliance obligations

- Industry-specific regulations

Risk Assessment Framework

Financial Risks:

- Revenue recognition issues

- Asset valuation problems

- Liability understatement

- Cash flow irregularities

- Foreign exchange exposure

Operational Risks:

- Internal control weaknesses

- Fraud and error possibilities

- System failure vulnerabilities

- Regulatory compliance gaps

- Key personnel dependencies

Compliance with IFRS and GAAP Standards

In Ireland, the accounting standards you follow depend on your company type and size.

What are these standards?

GAAP (Generally Accepted Accounting Principles): These are the general rules and guidelines for preparing financial statements.

IFRS (International Financial Reporting Standards): More detailed international standards used by larger companies and those trading internationally.

FRS 102: This is the main accounting standard used by most Irish companies. It’s a version of GAAP adapted for the UK and Ireland.

Which standard should you use?

Large Companies and PLCs:

- Must use IFRS if listed on a stock exchange

- Can choose between IFRS and FRS 102 if not listed

Medium and Small Companies:

- Typically use FRS 102 (full version or simplified Section 1A for small companies)

- Much simpler than IFRS with less complex disclosure requirements

Micro-Companies:

- Can use FRS 105, which is even more simplified

Technology & Automation in Audits

Digital Audit Solutions:

- Automated matching rules (up to 90% accuracy)

- Real-time anomaly detection

- Continuous monitoring systems

- AI-powered analysis tools

- Cloud-based audit platforms

Benefits:

- Reduced manual processes

- Enhanced accuracy rates

- Faster completion times

- Improved compliance tracking

- Better risk identification

Preparing for external audit success

Document Preparation:

- Review all expense claims for business purpose

- Ensure proper apportionment calculations

- Maintain detailed supporting records

- Check previous year corrections

- Implement simplified expense systems where appropriate

Process Improvements:

- Strengthen internal controls

- Enhance record-keeping systems

- Train staff on compliance requirements

- Regular internal audit reviews

- Professional advice engagement

Post-Audit follow up

Implementation Actions:

- Address audit recommendations promptly

- Update internal procedures accordingly

- Monitor compliance improvements continuously

- Schedule regular review meetings

- Maintain ongoing auditor communication

For the most accurate and up-to-date information on auditing standards and business record-keeping in Ireland, refer to the Irish Auditing and Accounting Supervisory Authority, Revenue.ie guidance on keeping records, and professional resources from Chartered Accountants Ireland.

Conclusion

In this blog we have covered the process of accounting audit in Ireland. The process will be covered from start to finish.

This guide helps Irish businesses get ready for accounting audits. We’ll walk you through the audit process from start to finish, show you what paperwork you need to have ready, and explain the different types of audits. You’ll also get helpful tips to stay on top of the rules. By following this guide, you’ll make sure your financial records are correct, clear, and ready to be checked. This helps you avoid common mistakes and shows your bank, investors, and partners that they can trust you.

Contact us today via call +353 212069255 or mail at info@outbooks.com.

FAQs about Accounting Audit

What are the 4 common phases in an accounting audit process?

A typical external or internal audit has four stages: planning, fieldwork, reporting, and follow-up. The accounting audit process ensures financial statements are examined thoroughly and accurately. This provides stakeholders with confidence in financial information reliability.

What are the 4 C’s of auditing?

The four C’s of internal audit are Compliance, Cybersecurity, Competitiveness, and Culture. However, these sets of 4 C’s are not universally defined or standardised. Different auditing in accounting frameworks may use variations.

What are the three key areas of auditing?

Financial statements, internal controls, and compliance are three key auditing areas. The focus areas can vary depending on audit nature and industry requirements. Audit and accounting objectives also influence area selection.

What are basic audit principles?

Confidentiality, integrity, objectivity, independence, and competence are basic audit principles. Auditors must follow these principles when conducting examinations. These principles ensure audits are conducted efficiently, effectively, and with complete integrity.

How often should Irish businesses conduct internal audits?

Irish businesses should conduct internal audit of accounts receivable and other areas annually. However, high-risk areas may require quarterly reviews. The frequency depends on business size, complexity, and regulatory requirements.

What documents are essential for an accounting audit in Ireland?

Essential documents include annual audited accounts, tax returns, bank statements, and general ledgers. You also need trial balances, invoice files, payroll records, and board meeting minutes. Financial audit checklist Ireland requirements may include additional industry-specific documents.

How can businesses prepare for HMRC expense claim scrutiny?

Businesses should review all expense claims for genuine business purposes. Ensure proper record-keeping with detailed mileage logs and receipts. Consider using HMRC simplified expense rates for easier compliance.

What is the role of the Irish Auditing and Accounting Supervisory Authority?

The Irish Auditing and Accounting Supervisory Authority oversees audit quality and compliance. They monitor statutory auditors and ensure adherence to professional standards. This authority plays a crucial role in maintaining audit integrity.

When is an external audit mandatory for Irish companies?

External audits are mandatory for public limited companies and certain private companies. Small companies may be exempt if they meet specific criteria. Audit requirements for businesses Ireland vary based on company size, turnover, and public interest considerations.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.