In Ireland, filing a self-assessment tax return means taking full responsibility for your own tax. There is no employer calculating what you owe, no automatic system checking your figures and Revenue acts on errors after they are submitted, not before.

The mistakes that appear most often in returns are not random. A form filed under the wrong threshold. Preliminary tax left unpaid in the first year. Reliefs available but never claimed. Each carries a financial consequence that grows the longer it remains unaddressed.

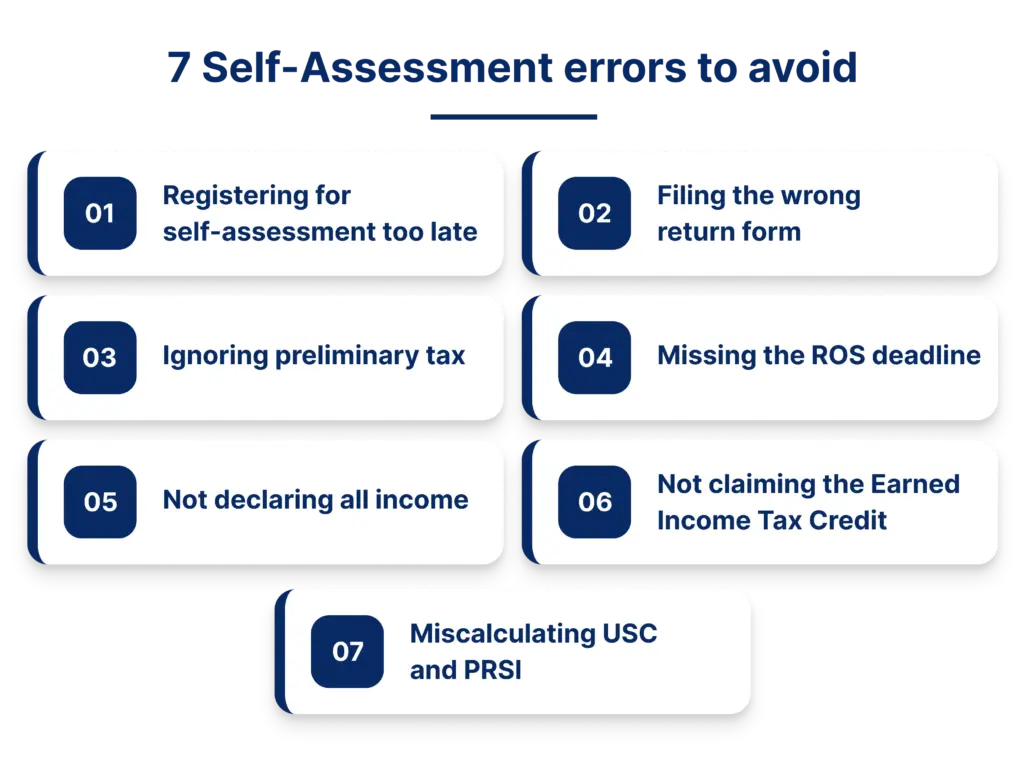

This blog covers who needs to file, the 2026 deadlines, the seven most common mistakes in Irish self-assessment returns and when professional support makes the most sense.

Key takeaways

- Form 11 requires two payments at once last year’s balance and an advance toward this year

- The November ROS deadline only applies when both filing and payment go through ROS

- The Earned Income Tax Credit of €2,000 for 2026 must be claimed on Form 11. Revenue does not apply it automatically

- USC and PRSI are calculated separately from income tax, so estimating only income tax may result in an incomplete total liability view

Who needs to file a Self-Assessment Tax Return in Ireland?

Self-assessment covers more than sole traders. Anyone earning income outside the PAYE system or earning above certain thresholds within it, may be required to file.

- Sole traders and freelancers: Anyone running a business or working independently with net non-PAYE income above €5,000 must register and file Form 11 annually.

- Landlords: Rental income is taxable in Ireland. Landlords earning above €5,000 net from property must file a self-assessment return regardless of other PAYE income.

- PAYE workers with additional income: A PAYE employee earning above €5,000 net from a side business, freelance work or any untaxed source must file Form 11.

- Directors: Company directors owning more than 15% of a company are classified as chargeable persons and must file Form 11 annually.

- Investors and those with foreign income: Dividend income, foreign earnings and certain investment returns above the threshold also require a self-assessment filing.

If you are unsure whether you need to file, registering for self-assessment through ROS using a TR1 form is the starting point.

What are the most common Self-Assessment Errors in Irish Returns?

Most people who file incorrectly are not ignoring their obligations. They are working from assumptions that do not reflect how the Irish self-assessment system actually works.

The seven mistakes below follow a logical sequence. Each one leads naturally into the next.

1. Registering for Self-Assessment too late

Registration with Revenue must happen as soon as a chargeable source of income begins, not at year-end. For a freelancer or sole trader, that means the month trading starts. For a landlord, it means the month rental income is first received.

Late registration does not pause the filing obligation. Revenue treats the return as late from the date income began, not from when you registered. Surcharges and interest apply from that point.

Registration is done through ROS using a TR1 form. Processing takes time and ROS access takes additional time to arrange. Leaving it until October creates unnecessary pressure before the filing deadline.

2. Filing the wrong return form

Form 12 applies when net non-PAYE income is below €5,000 and gross non-PAYE income is below €30,000. Once either figure is crossed, Form 11 is mandatory.

Being self-employed, a landlord or owning more than 15% of a company also makes Form 11 mandatory regardless of annual earnings.

Revenue does not notify you when this obligation begins. A person filing Form 12 in year one because income was below the threshold may continue doing so in year two without realising income has crossed it.

When Revenue identifies this, both years are reassessed, each carrying a late filing surcharge of up to 10% of the tax owed, plus daily interest.

3. Ignoring Preliminary Tax

Preliminary tax is an advance payment toward the current year’s Income Tax, PRSI and USC liability. It is due by 31 October each year.

When filing Form 11 in October, two payments are due at the same time. One clears the prior year’s balance. The other is preliminary tax for the current year. Both go through the same ROS screen on the same date.

People in their first year of filing have no prior figure to reference and must estimate 90% of the current year’s liability. Income in year one is rarely consistent, most people underestimate it and the result is a larger than expected combined payment in year two.

| Situation | Consequence |

| Preliminary tax underpaid | Interest charged on the shortfall from the due date |

| Preliminary tax not paid | Interest charged from the due date |

| Return filed late | Surcharge of 5% up to 56 days, 10% after |

Setting aside a percentage of each payment received throughout the year is the most practical way to manage this.

4. Missing the ROS deadline

Understanding the deadline correctly is as important as meeting it. There are two separate deadlines depending on how you file and pay.

| Filing method | Deadline for 2025 income |

| Paper return | 31 October 2026 |

| ROS filing and payment | 18 November 2026 |

To qualify for the extended deadline, both the return and the payment must go through ROS. Filing through ROS but paying by bank transfer loses the extension. Paying through ROS but submitting a paper return loses it as well.

Submitting a return before 31 August allows Revenue to calculate the liability on your behalf, removing the risk of a self-calculation error.

5. Not declaring all income

Every source of income belongs on Form 11. This includes main trade or rental earnings, PAYE wages, cash payments, informal jobs, income from short-term rental platforms, food delivery earnings and freelance platform payments.

Secondary income is not captured automatically. Each source must be entered in the correct panel on the form.

Revenue receives income data from multiple sources. Short-term rental platforms report host earnings directly to Revenue. Banks and payment processors share transaction records. PAYE income is already held by Revenue and cross-referenced against what is declared. Figures that do not align are queried.

The most reliable check before filing is to go through every bank statement and confirm each income entry appears on the return.

6. Not claiming the Earned Income Tax Credit

The Earned Income Tax Credit is worth €2,000 for the 2026 tax year. It reduces the income tax bill directly, not the taxable income and is the equivalent of the Employee Tax Credit that PAYE workers receive through payroll.

Unlike the Employee Tax Credit, it is not applied automatically. It must be claimed in the Charges and Deductions panel on Form 11.

Where both PAYE and self-employed income were earned in the same year, both credits can be claimed. The combined claim must stay within the €2,000 limit. If both are claimed without verifying this, Revenue may raise a query.

7. Miscalculating USC and PRSI

Income tax is not the only liability on a self-assessment return. USC and PRSI are calculated separately and add significantly to the total bill.

For the 2026 tax year, USC rates are:

| Annual income range | USC rate for 2026 |

| €0 to €12,012 | 0.5% |

| €12,013 to €28,700 | 2% |

| €28,701 to €70,044 | 3% |

| More than €70,044 | 8% |

| Self-employed income exceeding €100,000 | Additional 3% surcharge on the excess amount |

Note: For self-employed individuals, income above €100,000 is subject to an extra 3% USC surcharge, resulting in an effective USC rate of 11% on that portion of income.

Class S PRSI applies at 4.2% from January to September 2026, rising to 4.35% from 1 October 2026. Revenue applies a blended rate of 4.2375% when calculating annual liabilities for the 2026 tax year, with a minimum annual contribution of €650.

The mistake is estimating preliminary tax based on income tax alone and then facing an unexpected USC and PRSI liability at filing. For someone earning €60,000, USC and PRSI together can add several thousand euro to the total. Preliminary tax must account for all three charges.

Self-Assessment Tax Return Deadlines in Ireland 2026

Irish self-assessment does not operate on a single deadline. There are multiple dates, each tied to a specific filing method and each carrying different financial implications. The date that applies and what it costs when it passes, depends entirely on how the return is filed and how the payment is made.

| Deadline | Method | Date |

| Standard deadline | Paper return | 31 October 2026 |

| Extended deadline | ROS filing and payment | 18 November 2026 |

| Early filing option | ROS submission | Before 31 August 2026 |

What happens if you miss the deadline?

As confirmed in Revenue’s pay and file system guide, the surcharge is calculated as a percentage of the total tax liability for the year, not a flat fee.

- Filed within 56 days of the deadline: surcharge of 5% of the tax liability, capped at €12,695

- Filed more than 56 days late: surcharge of 10% of the tax liability, capped at €63,485

- Daily interest on unpaid tax from the due date at 0.0219%

A person with a €15,000 tax liability who files 30 days late faces a €750 surcharge in addition to the original bill. Filing two months late doubles that to €1,500, plus accumulated daily interest.

What to check before submitting your return?

- Confirm whether Form 11 or Form 12 applies based on total income for the year.

- Calculate preliminary tax separately from the prior year balance and budget for both.

- Ensure both the return and the payment go through ROS to qualify for the November deadline.

- Go through every bank statement and confirm all income sources are on the return.

- Claim the Earned Income Tax Credit in the Charges and Deductions panel on Form 11.

- Check rolling 12-month gross sales against the VAT threshold, not annual profit.

- Claim pension contribution relief on Form 11 if contributions were made during the year.

When does it make sense to use a Self-Assessment Tax Return Service?

Filing a return is manageable for those with a single income source and no significant changes year on year. It becomes considerably more complex when any of the following apply.

- First year of filing: No prior year figures for preliminary tax, unfamiliarity with ROS and a higher risk of underestimating the combined liability across income tax, USC and PRSI.

- Multiple income sources: Rental income, freelance earnings, dividends and PAYE income each have separate panels on Form 11 and separate rules for what is allowable.

- Prior years filed incorrectly: Revenue allows amended returns going back four years. In 2026, that covers 2022 through 2025. A self-assessment tax accountant can identify what was missed and file corrections before the window closes.

- Significant income growth: When income crosses thresholds for Form 11 or higher rate tax, the risk of error increases and the cost of getting it wrong grows accordingly.

A qualified accountant for self-assessment reviews the return before submission, ensures every relief is claimed and manages the ROS filing process. For most people, the cost of that review is less than the cost of a single missed credit or an avoidable surcharge.

For anyone uncertain about their position, professional tax advice before the October deadline is more cost-effective than correcting errors after Revenue has raised a query.

Conclusion

Most mistakes in a self-assessment tax return happen because people are not fully aware of all the rules and requirements. Since individuals are responsible for preparing and submitting their own returns, even small errors can lead to problems later. Revenue processes the information provided and by the time a query or correction notice arrives, interest and penalties may already have started to build up.

Reviewing your return carefully before submission can help avoid these issues. If your income has changed, your financial situation has become more complex or you think a previous return may contain errors, it is worth speaking with a qualified accountant before the filing deadline. This can help ensure your return is accurate and any potential issues are addressed early.

To discuss your self-assessment tax return, contact the Outbooks team at info@outbooks.com or call +353 21 206 9255.

FAQs

Who needs to file a self-assessment tax return in Ireland in 2026?

Anyone with net non-PAYE income above €5,000 must file Form 11. This includes sole traders, freelancers, landlords, directors owning more than 15% of a company and PAYE workers with significant additional income from any source.

How do I file a self-assessment tax return in Ireland?

Register on ROS, complete Form 11 declaring all income sources, calculate your liability across income tax, USC and PRSI and submit both your return and payment through ROS before the deadline. Payment is made through ROS alongside your return.

What happens if you miss the filing deadline in Ireland?

A surcharge of 5% of the total tax liability applies if the return is filed within 56 days of the deadline, rising to 10% after that. Daily interest at 0.0219% also applies on any unpaid tax from the original due date.

What is preliminary tax and how is it calculated?

Preliminary tax is an advance payment toward the current year’s income tax, USC and PRSI. The most practical calculation method is to pay 100% of the prior year’s total liability. First-year filers must estimate 90% of the current year’s expected liability.

How do you pay self-assessment tax in Ireland?

Payment is made through ROS using your digital certificate. Both the prior year balance and preliminary tax for the current year are paid together through the same ROS screen at the time of filing.

When should someone use a professional tax return service in Ireland?

Professional support is most valuable in the first year of filing, when income comes from multiple sources, when prior returns may have been filed incorrectly or when income has grown and thresholds have been crossed.

What is self-assessment bookkeeping and do I need it?

Accurate records of all income and expenses throughout the year are required for every self-assessment return. Revenue requires supporting documentation for every expense claimed and records must be kept for a minimum of six years.

Can I claim the Earned Income Tax Credit on my return in Ireland?

Yes, the Earned Income Tax Credit is worth €2,000 for the 2026 tax year and must be claimed in the Charges and Deductions panel on Form 11. It is not applied automatically and is one of the most commonly missed credits in Irish returns.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.