Last updated: May 2026

UK inflation continues reshaping how accounting firms approach pricing and proposal strategies in 2026. With rising compliance obligations, Making Tax Digital rollout, FRS 102 updates, and continued services inflation, accountants face mounting cost pressures that demand strategic pricing responses balancing profitability with client affordability.

Understanding how to adjust accounting proposal prices for UK inflation isn’t optional anymore it’s essential for practice survival. This guide will help you build inflation-resilient proposals that protect your margins whilst maintaining client relationships.

Key Takeaways:

- Current UK inflation rates (CPI 3.3%, March 2026) including services inflation at 4.5% – which hits accounting firms harder than headline figures

- Margin erosion risks from static fees vs. rising 5–7% costs in 2026

- Value-based pricing, inflation clauses, and fixed-fee escalators help protect profitability

- Proposal writing tips with adjustment language and scope definitions

- Client communication strategies for fee increases with timing and templates

- MTD for Income Tax is now live (April 2026) – how it justifies 15–25% fee increases for affected clients

- FRS 102 changes from January 2026 increasing limited company workload by 10–15%

The UK Inflation Landscape in 2026

The Office for National Statistics reports UK CPI at 3.3% in March 2026, up from 3.0% in February. CPIH (including housing costs) stands at 3.4%, whilst the Retail Prices Index sits at 4.3%. Importantly for accounting firms, services inflation is running at 4.5% – higher than the headline rate, meaning professional services costs are rising faster than general inflation.

The Bank of England said CPI inflation is likely to be around 3.1% in Q2 2026 and 3.3% in Q3, with higher energy prices still affecting the outlook. This means sustained cost pressure on accounting practices well into the 2026–27 financial year.

Food price inflation stands at 3.7% in March 2026, directly impacting household budgets and what clients can afford to pay for professional services.

For accounting firms, inflation affects more than utilities and software subscriptions. It impacts recruitment, retention, compliance delivery, cybersecurity spending, and client payment behaviour. Practices that fail to review pricing annually risk significant margin erosion over time.

How Inflation Impacts Accounting Service Costs

Accounting firms face compound cost pressures across multiple operational areas:

Staff Costs and Wages

Labour shortages drive wage inflation across professional services. To attract and retain qualified talent, many practices report wage increases between 4-7% annually often exceeding general inflation rates. This represents your single largest cost pressure.

Regulatory Compliance Workload

From 1 January 2026, updates to FRS 102 financial reporting standards introduced enhanced requirements around revenue deferrals, subscription income, and asset leasing. For limited company clients affected by these changes, accountant workload has increased by an estimated 10–15%, directly impacting the time and cost of service delivery.

Technology and Software

Cloud accounting software subscriptions typically increase 3-5% annually. Add practice management systems, cybersecurity tools, and compliance software, and technology costs compound quickly. Even maintaining your current tech stack costs more each year.

Professional Indemnity Insurance

Insurance premiums have climbed significantly, with many practices reporting 5-10% annual increases reflecting heightened claims activity and risk assessments.

Office and Operational Costs

Commercial property, utilities, and general office expenses all rise with broader inflation measures. Even hybrid working models don’t eliminate these pressures entirely.

The Margin Erosion Problem

Here’s the critical issue: when costs rise 4-6% annually but fees remain static, profit margins erode rapidly. A practice with 20% profit margins loses half its profitability within 3-4 years without fee adjustments. This makes pricing updates non-negotiable for sustainable operations.

Making Tax Digital for Income Tax: The Biggest Fee Justifier of 2026

From 6 April 2026, MTD for Income Tax Self Assessment (MTD ITSA) is now mandatory for sole traders and landlords earning over £50,000. This is the most significant change to UK accounting compliance in years — and your strongest justification for fee increases in 2026 proposals.

What Your Affected Clients Now Need

- Digital record-keeping using HMRC-compatible software (Xero, QuickBooks, FreeAgent)

- Four quarterly submissions to HMRC per year (instead of one annual Self Assessment)

- A final year-end declaration by 31 January

- Ongoing compliance monitoring throughout the year

The Fee Impact

Accountant fees for MTD-affected clients are expected to increase by 15–25% to reflect this additional workload. Annual Self Assessment clients effectively become year-round compliance clients.

MTD Rollout Timeline

- April 2026: Mandatory for income over £50,000

- April 2027: Threshold drops to £30,000

- April 2028: Threshold drops to £20,000

How to Reference MTD in Your Proposals

“Your fee reflects the move to MTD for Income Tax, which replaces your annual Self Assessment with quarterly digital reporting. This requires ongoing compliance support throughout 2026–27, not just at year-end.”

Why This Matters for Proposal Conversion

Instead of presenting fee increases as inflation-driven, successful firms position them as compliance-driven value enhancements. MTD gives accountants a strong justification to move clients from low-value annual billing models into higher recurring monthly packages.

Using proposal software with automated pricing templates and recurring service structures can significantly improve conversion rates during MTD onboarding conversations.

Pricing Strategy Options for Your Proposals

Different pricing approaches offer varying levels of inflation protection. Choose the model that fits your practice and client base.

Value-Based Pricing During Inflation

Value-based pricing ties fees to client outcomes rather than hours worked or costs incurred. This approach offers significant advantages during inflationary periods:

- Outcome Focus: Position fees around business value created tax savings, compliance certainty, strategic insights. When you quantify client benefits, pricing becomes less about your costs and more about their results.

- Natural Inflation Protection: As client businesses grow and their needs expand, value-based pricing scales naturally without awkward fee conversations every year.

- Higher Acceptance Rates: Clients more readily accept value-based pricing because it feels fairer. They’re paying for results, not absorbing your cost increases.

Consider tiered service packages (bronze, silver, gold) with clearly differentiated value propositions. Higher tiers include proactive services, faster response times, and strategic advisory components making the premium pricing obvious.

Inflation-Linked Pricing Clauses

Inflation-linked clauses provide automatic adjustment mechanisms that protect your margins systematically:

Clear Indexation: Reference specific indices like UK CPI or RPI. Specify whether increases apply annually, quarterly, or at contract renewal.

Reasonable Caps: Consider capping annual increases at 5-7% even if inflation exceeds these levels. Caps provide client certainty whilst still offering meaningful protection.

Sample Clause Language: “Fees are subject to annual review and may increase in line with UK CPI inflation. Any adjustment will not exceed the lower of actual CPI or 6% annually. We will provide 60 days’ notice of any fee changes before implementation.”

The key is transparency. Explain the mechanism upfront during proposal discussions. Clients appreciate predictability in professional relationships, even when it means gradual fee increases.

Fixed Fees with Built-In Escalators

Multi-year fixed-fee agreements with predetermined increases provide certainty for both parties.

Example

“Your fee for 2026-27 will be £2,500, increasing by 5% annually thereafter (£2,625 in 2027-28, £2,756 in 2028-29).”

This approach works especially well for compliance clients who value budgeting certainty.

When to Use Each Approach

Value-Based Pricing

Best for:

- Advisory-heavy clients

- Growth-focused businesses

- High-value service relationships

Inflation-Linked Pricing

Best for:

- Long-term compliance clients

- Monthly recurring engagements

- Larger client portfolios

Fixed Fee Escalators

Best for:

- Budget-conscious clients

- Multi-year engagements

- Stable recurring service models

2026 UK Accounting Fee Benchmarks

Use these figures to sense-check your proposals against current market rates:

| Client Type | Typical Annual Fee (2026) |

|---|---|

| Sole trader (simple) | £300 – £700 |

| Sole trader (with bookkeeping) | £700 – £1,200 |

| Freelancer / contractor | £400 – £900 |

| Small limited company | £800 – £1,800 |

| Ltd company (full service) | £1,800 – £2,500+ |

| VAT returns (add-on) | £400 – £1,200/year |

| Payroll per employee | £5 – £15/month |

| MTD ITSA uplift (affected clients) | +15% to +25% on base fee |

Source: 2026 UK market benchmarking. London-based firms typically charge 20–30% above these figures.

Writing Inflation-Resilient Proposals and Engagement Letters

Your engagement letters form the foundation for all future fee discussions. Build inflation protection in from the start.

Essential Components for 2026 Proposals

1. Fee Structure Clarity

Clearly specify whether pricing is:

- Fixed fee

- Monthly subscription

- Value-based

- Hourly

- Project-based

Also define exactly what’s included — and what falls outside scope.

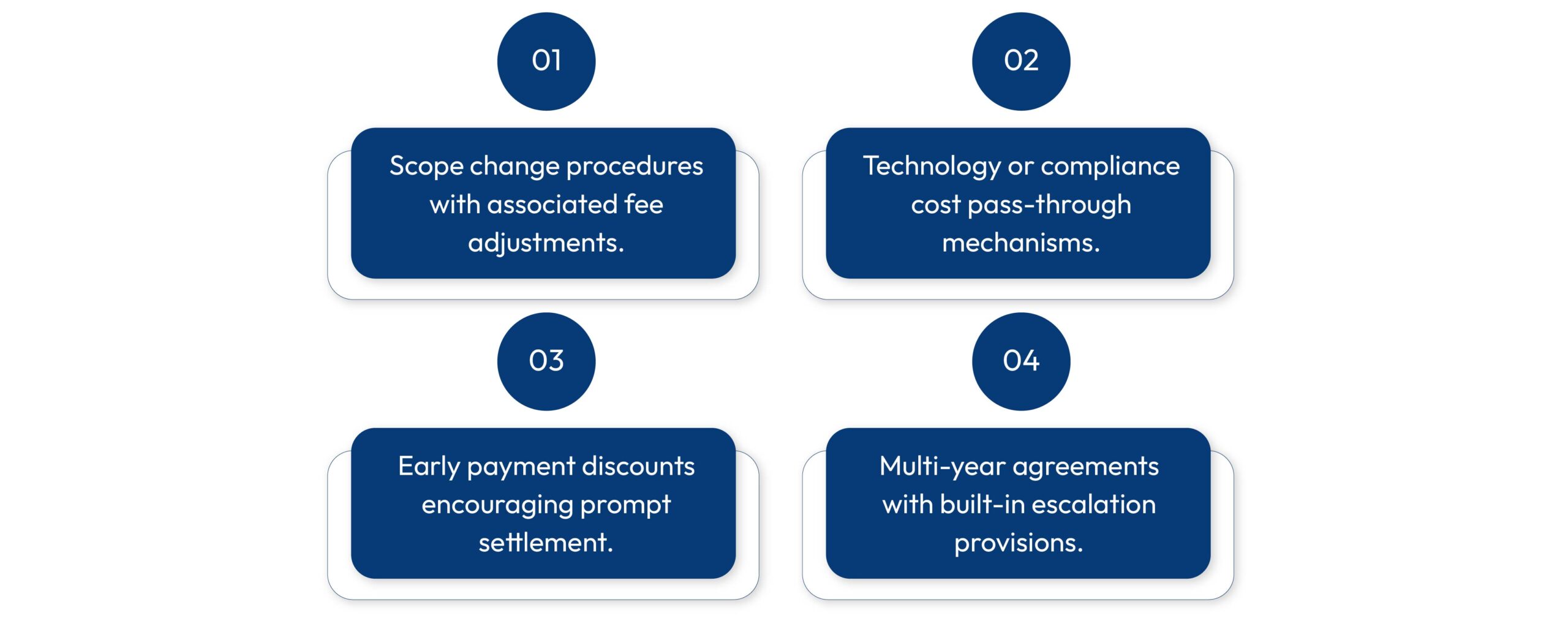

2. Scope Definitions

Strong scope wording protects profitability.

Example Scope Wording

“Fees quoted include standard bookkeeping, VAT returns, year-end accounts, and corporation tax submissions. Additional advisory, restructuring, MTD migration, or HMRC investigation work will be billed separately.”

3. Inflation Adjustment Language

Include pricing review clauses directly inside engagement letters.

Example

“Fees are reviewed annually in line with inflation, regulatory changes, and service scope adjustments.”

4. Compliance Change Clauses

This is increasingly important due to MTD and FRS 102 updates.

Example

“Where legislative or regulatory changes materially increase the scope of compliance work required, fees may be adjusted accordingly following client notification.”

5. Payment Terms

To improve cash flow during inflation:

- Encourage monthly direct debit payments

- Add early payment incentives

- Reduce long debtor days

Communicating Fee Increases to Clients

The way you communicate fee changes matters as much as the increase itself.

Clients respond better when fee increases are framed around:

- Increased compliance obligations

- Service improvements

- Technology upgrades

- Ongoing support requirements

- Regulatory complexity

Avoid positioning increases purely around “our costs went up.”

Best Timing for Fee Reviews

Most firms now review fees:

- At tax year-end

- During engagement renewal

- Before MTD onboarding

- After major compliance changes

Giving at least 60 days’ notice improves acceptance rates significantly.

Sample Client Email Template

Subject: Important Update Regarding Your Accounting Services for 2026–27

Dear [Client Name],

We’re writing to inform you of upcoming updates to your accounting service package for the 2026–27 financial year.

Looking ahead to 2026–27, like all businesses, we’ve experienced cost increases across staffing, technology, and operational expenses. UK services inflation is running at 4.5%, and the introduction of Making Tax Digital for Income Tax has also increased the compliance workload for many clients.

To continue providing proactive support, compliance monitoring, and reliable service standards, our fees will increase by 5% effective [date], in line with professional services cost increases and the additional compliance requirements introduced this year.

Your updated package will continue to include:

- Ongoing compliance support

- Digital bookkeeping guidance

- Year-round MTD assistance

- HMRC filing management

- Dedicated client support

If you have any questions regarding these changes, please contact our team.

Kind regards,

[Your Firm Name]

Final Thoughts

2026 is not just another inflation year for UK accountants. The combination of persistent services inflation, MTD for Income Tax, FRS 102 updates, and rising operational costs is fundamentally changing how accounting firms structure proposals and pricing.

Practices that proactively adapt pricing strategies, improve proposal clarity, and position compliance work as ongoing value services will protect margins and grow more sustainably.

The firms that continue using outdated fixed-fee models without annual reviews risk severe margin erosion over the next 2–3 years.

Now is the time to modernise your accounting proposals for the realities of 2026.

Frequently Asked Questions

How much should accountants increase fees in 2026?

Most UK accounting firms are implementing increases of 5–7% in 2026, reflecting both services inflation (4.5%) and the additional workload from MTD for Income Tax. For clients in scope of MTD ITSA, fee increases of 15–25% are justified. Consider UK CPI at 3.3% (March 2026) as your absolute floor – but services inflation at 4.5% is a more accurate benchmark for accounting practices.

Should accounting firms use inflation clauses in engagement letters?

Yes. Inflation-linked clauses reduce pricing friction by setting expectations upfront and allowing structured annual adjustments without full renegotiation.

Is value-based pricing better during inflation?

In many cases, yes. Value-based pricing protects profitability more effectively because fees are tied to client outcomes rather than internal delivery costs.

How often should accounting firms review pricing?

Most firms should review fees annually. However, MTD onboarding, major compliance changes, or significant scope increases may justify mid-year adjustments.

How does MTD for ITSA affect my accounting fees in 2026?

From April 2026, sole traders and landlords earning over £50,000 must file quarterly with HMRC instead of one annual Self Assessment. This increases your accountant’s workload significantly — four quarterly submissions plus a final declaration per year. Fee increases of 15–25% for affected clients are standard across the industry. If your income is between £30,000–£50,000, MTD becomes mandatory for you from April 2027.

What is services inflation and why does it matter for accountants?

UK services inflation is currently 4.5% (March 2026) — higher than the headline CPI of 3.3%. Since accounting is a service business, your costs (staff wages, software, insurance) are rising faster than general inflation. This is why a fee increase of 5% or more is reasonable even when clients point to the lower headline figure.

How do FRS 102 changes in 2026 affect my limited company clients’ fees?

FRS 102 financial reporting standards were updated from January 2026, introducing enhanced requirements for revenue recognition, subscription income, and asset leasing. For affected limited companies, preparation time has increased by an estimated 10–15%. If you have incorporated clients with these types of income streams, a scope review and fee adjustment is justified.