Account reconciliation is the process of comparing internal financial records against external statements, such as bank statements, invoices, or ledgers, to confirm that the figures match and the accounts are accurate.

For accounting teams managing multiple accounts or clients, reconciliation is what ensures financial data can be trusted. Unrecorded transactions, timing differences, and data entry errors are common, and without a structured reconciliation process, these issues are difficult to identify and correct before reporting deadlines.

This guide covers the main types of account reconciliation, a step-by-step process and best practices to help accounting teams reconcile accounts accurately and consistently.

Key Takeaways

- Account reconciliation checks internal records against external statements to make sure transactions are accurate.

- The process includes gathering documents, comparing transactions, investigating differences, making adjustments, and obtaining final approval.

- Matching individual transactions helps catch errors that checking balances alone can miss.

- Common types include bank, vendor, customer, and intercompany reconciliations.

- High volumes, inconsistent team practices, and audit requirements are common challenges.

- Clear procedures, prompt investigation, and proper documentation improve accuracy and reliability.

- Outsourcing reconciliation can help firms manage multiple accounts efficiently while allowing staff to focus on higher-value work.

Types of Account Reconciliations

Understanding the different types of reconciliations helps make the reconciliation process smoother and more accurate. Each type has its own focus and common issues:

Bank Reconciliation

Ensures that your general ledger matches the bank statement. Common items include outstanding checks, deposits in transit, or bank fees that haven’t been recorded yet.

Vendor Reconciliation

Confirms that what you owe matches supplier records. Missed invoices, duplicate entries, or timing differences often show up here.

Customer Reconciliation

Verifies that customer payments recorded in your books match what they actually paid. This helps catch overpayments, underpayments, or unapplied receipts.

Intercompany or Internal Reconciliation

Ensures transactions between departments or subsidiaries are consistent. Timing differences or missing entries are common challenges.

Credit Card Reconciliation

Confirms that credit card transactions in the general ledger match the monthly statement. Common issues include unrecorded charges, duplicate entries, and timing differences between when a charge is made and when it is posted.

Each type may use similar steps, but the focus shifts based on the account’s nature and common errors.

Step-by-Step Account Reconciliation Process

The account reconciliation process follows a consistent structure across account types. In practice, it moves step by step, with each stage helping reduce differences until the final balance is clear and reliable for reporting.

Step 1: Gather and Organize Documents

Start by gathering the general ledger for the period along with the relevant external records, such as bank statements, vendor statements, or supporting schedules. Both should cover the same period before any comparison begins.

Many issues begin here. If the general ledger is not fully updated but the external statement is already finalized, the differences that appear are often due to timing, not actual errors. This can lead to unnecessary investigation.

Before moving forward, check that:

- Both records cover the same period

- No late entries affect the comparison

If this step is skipped, the rest of the reconciliation may not be reliable.

Step 2: Compare Balances and Check Transactions

Once the records are ready, start by comparing the opening and closing balances. After that, check transactions one by one to make sure both records reflect the same activity.

Looking only at totals can be misleading. Sometimes balances match even when there are errors, especially if one error offsets another.

Focus on finding differences. Any transaction that appears in one record but not the other should be noted and carried forward for review.

Step 3: Identify and Group Differences

After identifying differences, group them into categories such as timing differences, errors, or items requiring further investigation,

Some differences are normal, especially those caused by timing gaps between systems. Others may point to missing entries, duplicate records, or incorrect posting.

Pay attention to items that repeat across periods or remain unresolved. These usually indicate systemic issues that require investigation.

Step 4: Investigate Differences and Find the Cause

At this stage, the goal is to understand why each difference exists. Each item should be traced back to its source using supporting documents such as invoices, payment records, or journal entries.

This is often the most time-consuming part of the account reconciliation process. The aim is not just to find the difference, but to understand how it happened.

If a difference cannot be resolved within the close cycle, it should be escalated instead of being carried forward.

Step 5: Record Adjustments and Finalize Records

Once the cause is clear, record the necessary corrections through proper journal entries, each supported by clear documentation.

The reconciliation should now show how the final balance has been reached, with all differences either resolved or clearly explained.

Recording adjustments without fully understanding the root cause can introduce new errors and make future reconciliations harder to resolve.

Step 6: Review, Approve, and Close

The final step is to review the reconciliation to make sure everything is complete and accurate.

Before closing, confirm that:

- All differences are resolved or explained

- Records are properly documented

- The reconciliation is ready for review

A matching balance alone is not enough. The process is complete only after it has been reviewed and approved.

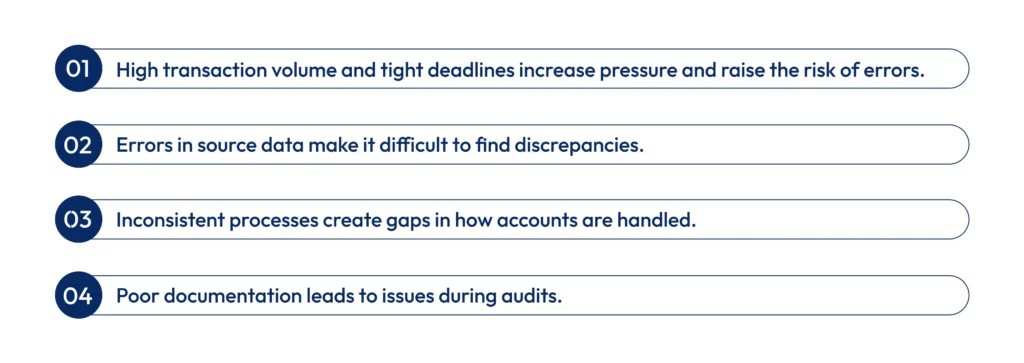

Common Challenges in the Account Reconciliation Process

Even with a clear process, reconciling accounts can be difficult in practice. Accounting teams often face recurring issues that slow down month-end close and increase the risk of errors.

For firms managing multiple clients, these challenges are amplified. Firms like Outbooks support accounting teams by handling reconciliation consistently across accounts, helping reduce errors and allowing internal staff to focus on review and analysis instead of repetitive tasks.

Best Practices for Effective Account Reconciliation

Accounting teams often face tight deadlines, high transaction volumes, and recurring discrepancies. Applying structured practices helps reduce errors, maintain consistency, and improve confidence in financial reporting.

1. Maintain Accurate and Complete Records

- Update the general ledger and all supporting documents such as invoices, bank statements, and vendor statements, before reconciliation. Outdated or incomplete data creates unnecessary reconciling items and slows the process.

- Ensure every entry has sufficient detail. Missing transaction references or unclear descriptions make investigation harder and increase the risk of misclassification.

2. Match Transactions, Not Just Balances

- Comparing only opening and closing balances can hide errors. Match each transaction individually to uncover duplicates, missed entries, or misposted amounts.

- Focus on high-risk accounts, like cash, accounts receivable, and credit cards, where errors are more frequent. This prevents small mistakes from becoming material misstatements.

3. Categorize Reconciling Items Thoughtfully

- Separate unmatched transactions into timing differences, posting errors, or items that need investigation. Proper categorization prevents minor discrepancies from consuming unnecessary time.

- Document why each item falls into its category. This ensures anyone reviewing the reconciliation understands the issue and avoids repeated confusion.

4. Investigate Unresolved Items Promptly

- Trace every unexplained transaction to its source invoice, payment confirmation, journal entry, or bank notice. Delaying investigation increases risk of errors being carried forward.

- Escalate items that cannot be resolved quickly to a senior accountant or manager. Early escalation prevents last-minute surprises during month-end close.

5. Standardize Procedures Across Team Members

- Clearly document reconciliation steps for each account type and ensure all staff follow the same approach. This reduces variations and preserves institutional knowledge when team members change or accounts are reassigned.

- Include decision points for escalation, materiality thresholds, and categorization standards so everyone knows exactly how to handle reconciling items.

6. Document and Archive Thoroughly

- Keep full records, including opening balances, reconciling items with explanations, and final balances. A balance alone does not confirm accuracy.

- Maintain a consistent sign-off and archival process. Well-documented reconciliations support audits, reduce repeated errors, and make future reconciliations faster.

7. Regularly Review and Improve the Process

- Analyze recurring discrepancies or bottlenecks to identify improvement opportunities. Adjust categorization, investigation methods, or workflow sequencing based on patterns observed.

- Collect feedback from team members who perform reconciliations. Practical insights from daily work can reveal subtle inefficiencies that generic rules miss.

Conclusion

Account reconciliation is not complicated when the right process is in place. Gathering the correct documents, matching transactions individually, investigating discrepancies promptly, and documenting everything thoroughly are what make reconciliations accurate, consistent, and audit-ready.

The firms that struggle are usually those without a standardized workflow, where practices vary between team members or accounts are left unreconciled until deadlines force the issue. A repeatable process fixes this and makes month-end close far more manageable.

To see how Outbooks can support your firm in making reconciliations smoother and more reliable, call us at +1 386 251 5318 or email info@outbooks.com.

FAQs

What is account reconciliation?

What software tools are used for account reconciliation?

How does reconciliation differ for small businesses vs. large enterprises?

Is reconciliation the same as an audit?

What happens if discrepancies are not resolved?

How does outsourcing reconciliation maintain data security?

How to reconcile accounts?

What is the bookkeeping reconciliation process?

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.