Auditing as a profession has reached a important decision point. Standard-setters together with regulators and users have started to doubt the trustworthiness of traditional audit methods.

Multiple upcoming market trends are set to transform audit practices in 2025-26 thus changing the market value provided by audits. Let us have a look at the future of accounting profession below:

Note : This article was originally published in 24 April 2025 and last updated on 18 March 2026 to reflect the AICPA 2025 AI in Accounting Report findings, the emerging ‘digital senior’ role, the CPA talent shortage data, and the shift from AI experimentation to AI operationalization in 2026.

Key Takeaways

- Trust is falling – only 62% of investment professionals trust audit opinions today, down from 73% in 2019.

- AI is now operational, not experimental – firms using AI workflows are already outpacing those still testing.

- The digital senior is the new must-have role – part accountant, part AI manager.

- 300,000+ accountants have left since 2020 – firms are replacing headcount with AI, not new hires.

- ESG assurance is the fastest-growing audit segment – climate, supply chain, and cybersecurity now sit alongside financial statements.

- The SEC stepped back in 2025 – mandatory climate rules vacated, but investor and California state demand keeps ESG reporting going.

- AI won’t replace accountants – it handles volume; humans handle judgment, ethics, and strategy.

Crisis of confidence

The audit profession faces a crisis of confidence from multiple directions. IFIAR inspection data reveals 30% of audits examined contain significant deficiencies.

Financial reporting fraud causes estimated global losses of $4.7 trillion annually according to ACFE research.

A 2023 CFA Institute survey found only 62% of investment professionals trust audit opinions, down from 73% in 2019.

Technology revolution

The technological transformation of audit is now well underway in 2026:

| Technology | Adoption Rate | Key Impact |

|---|---|---|

| Advanced Analytics | 78% | Full population testing replaces sampling |

| AI-Powered Risk Assessment | 65% | 40% reduction in risk assessment hours |

| Continuous Auditing | 64% | Move from annual to real-time assurance |

| Blockchain Verification | 45% | Automated confirmation of transactions |

Technology revolution is one of the important aspect of future of accounting profession.

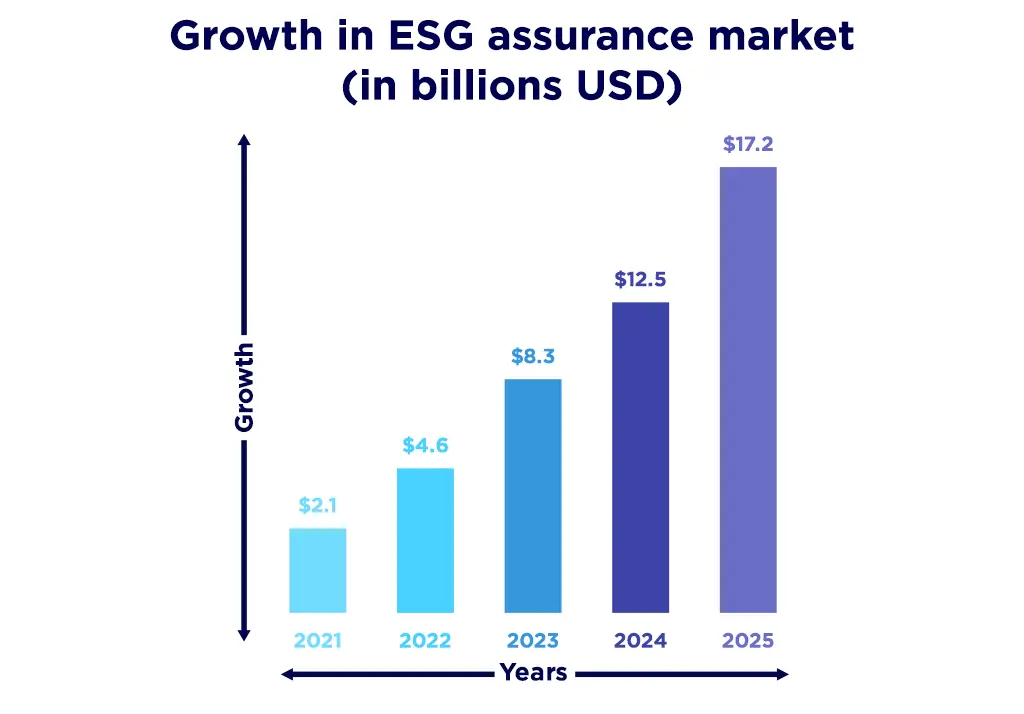

Beyond financial statements

ESG assurance represents the fastest-growing segment in the audit profession. Market size is projected to reach $17.2 billion by 2025.

Regulatory drivers include the SEC’s climate disclosure rules and the EU’s Corporate Sustainability Reporting Directive.

Future of auditors will provide assurance on multiple dimensions beyond traditional financial reporting:

Expansion of Assurance Services by 2025

| Assurance Area | Growth | Key Drivers |

|---|---|---|

| Integrated Reporting | +65% | Investor demand for holistic reporting |

| Climate Risk | +87% | TCFD-aligned mandatory disclosures |

| Supply Chain Ethics | +125% | Modern slavery legislation expansion |

| Cybersecurity | +45% | SEC cybersecurity disclosure requirements |

Future of auditing includes various types of auditing, like future of internal audit, external audit and more.

Talent transformation

The audit professional of 2025 requires a dramatically different skill set. Firms are actively recruiting from diverse academic backgrounds.

Research shows 40% of new hires at major firms will come from non-accounting backgrounds by 2025.

Data science has become a core competency for modern auditors. PwC’s Digital Academy has trained over 50,000 staff in advanced data skills.

Behavioral science expertise helps assess culture and conduct risks. Deloitte has embedded behavioral scientists in 35% of its largest audit engagements.

Environmental scientists verify sustainability claims with scientific rigor. KPMG has hired over 2,000 climate scientists and sustainability experts since 2021.

Evolution of Audit Team Composition

| Professional Role | 2020 | 2025 (Projected) | Key Skills Required |

|---|---|---|---|

| Traditional Auditors | 85% | 60% | Accounting, professional judgment |

| Data Scientists | 5% | 15% | Advanced analytics, programming |

| IT/Systems Specialists | 8% | 12% | IT controls, cybersecurity |

| ESG Specialists | 1% | 8% | Sustainability frameworks, environmental science |

| Behavioral Experts | <1% | 5% | Psychology, culture assessment |

Another important aspect of future of accounting profession is value proposition evolution.

Value proposition evolution

Leading firms have reimagined their value proposition beyond compliance. Audit is increasingly valued for its strategic insights.

Forward-looking risk identification has become a key differentiator. Top firms identify emerging risks 14 months before they materialize on average.

McKinsey research shows strategic audits deliver 2.3x more actionable insights than compliance-focused engagements.

Enhanced stakeholder trust translates to tangible financial benefits. Companies with high-assurance services experience 12% less stock price volatility.

Audit market transformation

U.S. regulators are focusing on audit quality and fraud detection. PCAOB enforcement actions have increased 215% since 2020.

The UK is implementing reforms following the Brydon Review. Big Four firms face mandatory separation of audit from consulting services by 2025.

Enhanced joint audit requirements are being implemented across the EU. This creates opportunities for mid-tier audit firms to gain market share.

Traditional audit fees are rising at approximately 3.5% annually. This reflects efficiency gains offsetting increased regulatory requirements.

ESG assurance commands premium pricing, with fees growing 25-30% annually. This growth is driven by specialized expertise requirements and limited supply.

Regulatory evolution

The regulatory landscape will continue evolving through 2025. New assurance standards are maturing rapidly.

The IAASB’s Extended External Reporting (EER) framework covers 12 distinct assurance domains.

Independence requirements are adapting to new realities. IESBA has developed specific independence rules for non-financial assurance engagements.

Quality management is shifting to outcomes-based assessment. ISQM implementation affects over 5,000 audit firms globally.

Global convergence is accelerating as capital markets demand consistency. The gap between U.S. GAAS and International Standards on Auditing continues to narrow.

Key Regulatory Developments Impacting Audit (2023-2025)

| Region | New Regulation/Standard | Implementation | Primary Impact |

|---|---|---|---|

| Global | ISQM 1 & 2 Full Implementation | January 2025 | Quality management systems overhaul |

| US | SEC Climate Disclosure Rules | 2024-2025 | Mandatory climate risk assurance |

| EU | CSRD Reporting Requirements | 2024-2026 | Comprehensive sustainability assurance |

| UK | Audit & Assurance Policy | January 2025 | Expanded board responsibility |

Note : The SEC vacated its mandatory climate disclosure rules in February 2025. ESG reporting demand continues – driven by institutional investors and California’s state-level requirements. (Source: Accounting Today, 2025)

New assurance standards are maturing rapidly. The IAASB’s Extended External Reporting (EER) framework covers 12 distinct assurance domains.

Independence requirements are adapting to new realities. IESBA has developed specific independence rules for non-financial assurance engagements.

What’s Changing in the Accounting Profession in 2026

AI has moved from experimentation to execution.

2026 marks a clear dividing line between firms that merely own AI tools and those that have built them into daily workflows. The emerging role of the “digital senior” – an accountant who blends technical expertise with AI oversight and workflow design – is becoming one of the most valued positions in the profession. (Source: CPA Practice Advisor, December 2025)

The CPA shortage is accelerating the shift.

Over 300,000 accountants have left the profession since 2020, and AICPA estimates 75% of today’s CPAs will retire within the next 15 years. Rather than hiring to fill the gap, firms are deploying AI to expand capacity without growing headcount. Accounting Today’s 2026 Year Ahead survey found 35% of firms plan to automate core processes using AI this year. (Source: Accounting Today, February 2026)

AICPA’s position is clear.

In its 2025 AI in Accounting Report, AICPA confirmed: “AI is not going to disrupt the accounting profession, but it will change what an accountant does.” Firms further ahead in adoption are already shifting away from hourly billing toward high-value advisory services – using AI to handle volume so professionals can focus on judgment and strategy. (Source: CPA.com / AICPA, June 2025)

Agentic AI is the next frontier.

Platforms from Thomson Reuters and Wolters Kluwer now automate tax preparation and document analysis end-to-end – with professionals reviewing outputs rather than building them from scratch. In audit, tools like Trullion and DataSnipper are embedding AI directly into evidence gathering and exception flagging, further reducing time spent on routine procedures.

Your Trusted Outsourced Accounting Partner.

Get Started TodayConclusion

The audit profession is undergoing profound transformation. Changes in technology, scope, and value are reshaping the field through 2026 and beyond.

The future of the accounting profession depends on leveraging technology to eliminate routine tasks, enabling focus on judgment and strategic value.

Expanded assurance domains create unprecedented career opportunities. Tomorrow’s audit leaders will work across disciplines and industries.

For organizations embracing these changes, the future of auditors is extraordinarily promising. The transformation will create new value for clients, professionals, and capital markets.

FAQs about future of Accounting Profession

What are the biggest trends transforming the accounting profession in 2025/26?

AI and automation, ESG assurance, cybersecurity reporting, and a growing CPA talent shortage. Firms already running AI workflows are pulling ahead of those still experimenting.

How will AI change auditing and accounting by 2026?

AI handles data gathering, anomaly detection, and routine compliance – freeing accountants for analysis and advisory. As AICPA puts it: AI will change what an accountant does, not eliminate the profession.

What happens to internal audit as automation expands?

Internal auditors shift from checklist reviewers to strategic advisors. Automation handles routine testing; humans handle judgment, interpretation, and risk intelligence.

How often should companies audit their accounts in 2026?

High-risk processes move toward continuous auditing; lower-risk areas stay quarterly or annual. Real-time monitoring now supplements mandatory annual filings rather than replacing them.

Can AI fully replace accountants and auditors?

No. Volume and pattern recognition – yes. Professional judgment, ethical reasoning, and stakeholder communication – no. The 2026 model is human-AI collaboration, not replacement.

What skills do accountants need for 2025/26?

Data literacy, AI tool proficiency, ESG reporting knowledge, and advisory communication. AICPA’s Profession Ready initiative is directly addressing the early-career skill gap AI is creating.

Is the accounting profession facing a talent shortage?

Yes – seriously. Over 300,000 accountants left since 2020 and 75% of current CPAs are approaching retirement. Firms are using AI to offset the shortfall while enrollment slowly recovers. (Source: AICPA / Workday, 2025)

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.