When it comes to accounting, the two main methods are cash basis and accrual basis accounting. The best choice between the two depends on the size of the business, its structure, and its financial needs.

Cash basis is a good option for small businesses with simple transactions, whereas accrual accounting is more suitable for businesses with inventory, credit sales, or those who need a clear understanding of their finances over time.

In both methods, the same transactions are recorded. The difference lies in the timing of when they are recorded and that timing affects your financials and how reliably you can use them to make decisions.

Key takeaways

- The real difference between accrual vs cash accounting is not just timing, it is how your financials actually reflect your business activity.

- Cash basis shows what has been paid and received, but it can miss unpaid invoices, pending bills, and the reporting gaps caused by payment timing.

- Accrual accounting records revenue and expenses in the same period, which gives you more accurate monthly financials.

- The choice of method affects how your revenue, profit, trends appear across different periods.

- Businesses with average annual gross receipts above $32 million must use the accrual method under IRS rules.

- Switching between methods is not automatic and requires filing IRS Form 3115 with approval.

Key differences between Accrual and Cash Basis Accounting

The difference between cash and accrual accounting goes beyond when transactions are recorded. Each method affects how revenue, expenses, and overall business performance appear in your financial reports.

| Feature | Cash Basis Accounting | Accrual Accounting |

|---|---|---|

| Revenue Recognition | Recorded when payment is received | Recorded when income is earned |

| Expense Recognition | Recorded when payment is made | Recorded when expenses are incurred |

| Accounts Payable & Receivable | Not typically tracked | Fully tracked |

| GAAP Compliance | No | Yes |

| IRS Eligibility | Allowed for eligible small businesses | Required for corporations/partnerships with average annual gross receipts above $32 million |

| Best Suited For | Small businesses with simple transactions | Businesses with inventory, credit sales, or long-term growth plans |

Revenue and expense timing

Cash basis records income when the payment is received and expenses when they are paid. It follows the movement of cash, nothing more.

Accrual accounting records income when it is earned and expenses when they occur, even if the payment has not been made yet.

For example: If you send a $10,000 invoice in December and the payment is received in March, cash basis will record it in March when the payment is actually received. However, under accrual accounting it is recorded in December itself. As a result, your monthly performance can look very different depending on which method you follow.

The matching principle

Accrual accounting follows the matching principle, it records expenses in the same period as the related revenue. This gives a clearer picture of how that period actually performed.

Cash basis does not follow this principle. It records income and expenses only when the cash is received or paid. This can place related transactions in different periods and make profits look inconsistent.

Accounts Receivable and Accounts Payable

Accrual accounting uses both. Accounts receivable tracks what customers owe you. Accounts payable tracks what you owe vendors.

Cash basis uses neither. If you have $50,000 in unpaid invoices, your books show none of it.

Unearned revenue and prepaid expenses

Let’s assume a client pays $12,000 upfront for a year-long service. Accrual records it as a liability and recognizes $1,000 each month as the service is delivered. Cash basis records the full $12,000 as income on day one.

The same applies to prepaid expenses. A $12,000 annual software subscription paid in January is spread across 12 months under accrual. Cash basis records it all in January.

Asset cost and depreciation

Accrual spreads the cost of an asset over its useful life through depreciation. Cash basis records the full cost in the period you pay for it. This can create a large expense in one period that does not reflect actual performance.

Seasonal distortion

A retailer on cash basis may look very profitable in Q4 and unprofitable in Q1 not because the business changed, but because cash flow is uneven. Accrual puts revenue and expenses in the right periods, giving consistent financials all year.

Pros and Cons of Cash Basis Accounting

Cash basis works well when your transactions are simple and you get paid quickly. But it has real gaps that become more noticeable as your business grows.

Pros

- Easy to manage with very little bookkeeping

- Shows exactly how much cash you have right now

- Gives you flexibility in managing taxable income you can time when you receive or make payments

- This is usually less expensive because it involves fewer adjustments and simpler bookkeeping.

Cons

- Outstanding invoices and unpaid bills do not show in your books

- Profitability figures can be misleading, especially with payment delays or seasonal revenue

- Full asset costs recorded at purchase can distort your profit figures

- Not GAAP compliant which limits your access to most lenders and investors

- Does not handle prepaid expenses, unearned revenue, or long-term contracts accurately

Pros and Cons of Accrual Accounting

Accrual accounting gives you a more complete and reliable view of how your business is doing. That accuracy requires more effort to maintain.

Pros

- Gives accurate, period-specific financials

- Required for GAAP compliance needed for investors, lenders, and audits

- Handles unearned revenue, prepaid expenses, and depreciation correctly

- Shows a full picture of what you owe and what is owed to you

- Removes distortions caused by uneven cash flow or seasonal revenue

Cons

- More work to maintain requires tracking receivables, payables, and adjustments

- Can show profit on paper while actual cash is tight

- It generally costs more due to the added tracking of receivables, payables, deferred revenue, depreciation, and monthly adjustments.

- Income is recognized before payment arrives, which can lead to unexpected tax bills

Which Accounting software supports Cash and Accrual Accounting?

Most modern accounting platforms support both methods, although accrual features are usually more advanced in higher-tier plans.

Popular options include:

These platforms can generate both cash basis and accrual basis reports, making it easier for businesses to manage taxes and financial reporting separately.

IRS and GAAP requirements

Your accounting method is not always your choice. The IRS and GAAP both set rules based on your business size, structure, and reporting needs.

IRS rules

Under current IRS rules, businesses with average annual gross receipts of $32 million or less over the previous three tax years can generally use the cash method of accounting. This threshold is adjusted annually for inflation verify the current year’s figure at IRS.gov before making any accounting decisions.

C-corporations and partnerships with a C-corporation partner may face additional restrictions regardless of their revenue size.

GAAP requirements

GAAP requires accrual accounting. If your business needs audited financial statements for investors, lenders, or regulators you must use accrual. Publicly traded companies filing with the SEC are required to follow GAAP.

Nonprofits

Most nonprofits are not legally required to use accrual accounting. Smaller nonprofits may use cash basis. However, accrual is required for GAAP compliance which applies when a nonprofit needs audited financial statements, certain grants, or lender funding.

Tax vs Reporting

A business can file taxes on a cash basis and maintain accrual books for reporting purposes. This is a practical option for smaller businesses that want tax flexibility without losing reporting accuracy.

Which is better Accrual vs Cash Accounting for small businesses?

If your business has simple operations and stays below the IRS threshold, cash basis accounting is usually the easier and more cost-effective option.

Accrual accounting becomes more useful when businesses need detailed financial reporting, manage inventory, or work with investors and lenders.

Below is a clear guide to help you decide.

Choose Cash basis accounting method if:

- You run a small, service-based business with no inventory

- You get paid quickly with no extended credit terms

- Your gross receipts are below $32 million

- You do not need GAAP-compliant reports for lenders or investors

- Keeping accounting simple and low-cost is important

Choose Accrual basis accounting method if:

- You carry inventory or sell on credit

- You work on long-term projects or contracts

- Your gross receipts are at or above $32 million

- You need GAAP-compliant reports for audits, investors, or lenders

- You want accurate monthly financials that are not affected by payment timing

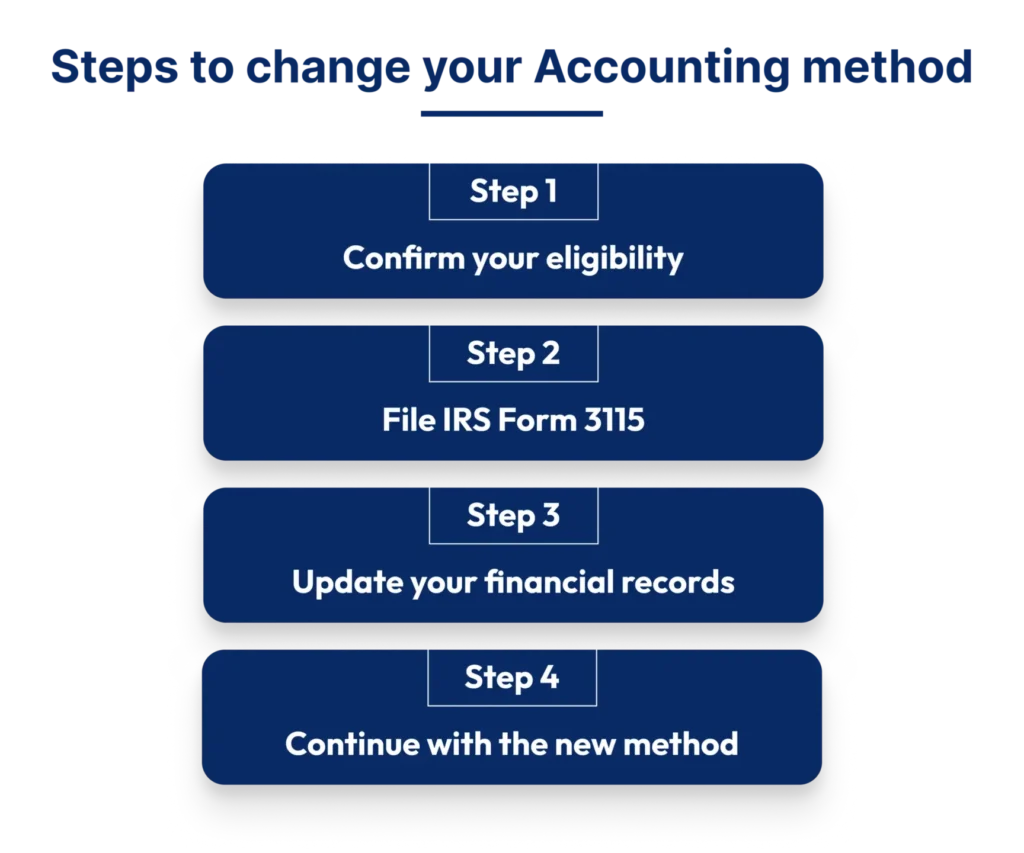

How to switch your Accounting method?

Switching is possible but it requires a formal process. You cannot simply change methods at the start of a new year.

Step 1: Check eligibility requirements

Most common switches (such as cash to accrual or accrual to cash) qualify as automatic changes under IRS procedures. Check the IRS List of Designated Automatic Accounting Method Change Numbers (DCNs) in the Instructions for Form 3115 to confirm which category applies to you.

Step 2: File IRS Form 3115

File Form 3115 in the tax year you want the change to apply.

- Automatic change: No advance IRS approval or user fee is required. Attach the original Form 3115 to your timely filed federal tax return for the year of change, and send a signed duplicate copy to the IRS in Ogden, UT. Consent is granted automatically upon proper filing.

- Non-automatic change: Submit Form 3115 to the IRS National Office during the tax year. A user fee applies and formal written IRS approval is required before implementing the change.

Step 3: Update your financial records

Update your books to reflect the new accounting method. This may include recording unpaid invoices, outstanding expenses, deferred revenue, and other previously untracked items, along with any required Section 481(a) adjustment to account for the cumulative effect of the change.

Step 4: Continue with the new method

After the switch, all future reporting and tax filings must consistently follow the new accounting method.

Your Trusted Outsourced Accounting Partner.

Get Started TodayConclusion

Cash basis is a practical option for businesses with simple transactions where recording payments as they happen is enough.

Accrual accounting records income and expenses in the period they relate to, not just when payments are made, which gives you a better understanding of your performance.

The choice significantly depends on how your business operates and how much clarity you need from your financials.

At Outbooks, we help US businesses set up the right accounting method and support them when a change is needed. Contact Outbooks at info@outbooks.com or call us at +1 386 251 5318 for a consultation.

Frequently Asked Questions

Which is better cash or accrual accounting?

It depends on your business. Cash basis suits small service businesses with simple transactions. Accrual suits businesses with inventory, credit sales, or external reporting needs like investor or lender requirements.

What is the IRS threshold for requiring accrual accounting?

Businesses with average annual gross receipts above $32 million over the prior three years must use accrual.

Can a business use cash basis for taxes and accrual for reporting?

Yes, you can file taxes on a cash basis and maintain accrual books for reporting. This gives tax flexibility without affecting the accuracy of your financial reports.

Is there a hybrid accounting approach?

Some businesses use a hybrid method that combines elements of cash and accrual accounting. For example, inventory may be tracked using accrual while other transactions follow cash basis.

How do I switch from cash basis to accrual?

File IRS Form 3115 in the tax year you want to switch. IRS approval is required and is not guaranteed. Prior financial records must also be updated to reflect the new method.

What happens if I use the wrong accounting method?

Using an incorrect accounting method can create reporting inaccuracies, tax filing issues, and possible IRS penalties if your business does not meet eligibility requirements.

What are the GAAP requirements for accounting methods?

GAAP requires accrual accounting. Any business that needs audited financial statements for investors, lenders, or regulators must use the accrual method.

Is accrual accounting better for seasonal businesses?

Yes, accrual puts revenue and expenses in the periods they belong to. This removes the profit distortions that cash basis creates when revenue is uneven across the year.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.