The pressure to maintain accurate financial records is increasing day by day. Business owners face this mounting pressure, which makes it difficult for them. Modern complexity and regulations are not fulfilled by the traditional bookkeeping methods.

A recent study shows that 29% of the companies have already adopted accounts payable process to increase accuracy.

Common bookkeeping mistakes are accelerating without proper system and knowledge. The risks of uncertain legal complications and finances rises with these errors.

72% of accounting and bookkeeping practices reported increased revenue in the past 12 months, indicating strong market demand for professional services.

With outsourcing bookkeeping internal errors are eliminated and strategic financial insights are also provided. Professional services offer technology and expertise that small businesses in the U.S. cannot afford internally.

This comprehensive guide explores critical bookkeeping errors and how professional outsourcing prevents them.

Understanding common Bookkeeping mistakes

When business owners lack proper training or systems it results in bookkeeping errors. These mistakes start with simple data entry mistakes to intricate sorting issues.

Small business bookkeeping mistakes spring from inadequate time allocation. Busy owners focus more on sales over financial record-keeping. This leads to long term problems that can be easily prevented by outsourcing.

Accurate bookkeeping gets even more critical due to the complex U.S. tax regulations. Professional grade accuracy is the topmost priority in financial records which modern businesses require. This expert skill can be achieved without hiring full time staff with outsourcing.

The 5 most common Bookkeeping mistakes

While basic mistakes like poor record-keeping, improper expense categorization, and skipping bank reconciliation are commonly known, there are deeper, more costly errors that are unnoticed.

These overlooked mistakes often begins from business growth, technology gaps, and changing regulations.

Unlike simple data entry errors, these mistakes can drain your profits for months before you notice them. They’re the difference between a successful business and one that struggles despite good sales.

1. Missing to track the timely revenue recognition

Recording revenue after receiving payment, messes up the cash flow. The business decisions are truly affected with the timing difference between earning revenue and collecting as is vital.

When service contracts paid annually but delivered monthly it creates false cash peaks. Forecasting becomes difficult for subscription businesses when they mix setup fees with monthly revenue.

| Type of revenue | Problem | Solution |

|---|---|---|

| Annual contracts | Fake cash peaks | Track the monthly earnings separately |

| Subscriptions | Improper forecasting | Separate setup fees from recurring revenue |

| Construction | Low working capital | Record revenue as work progresses |

2. Ignoring accrued liabilities and hidden costs

Beyond basic expense tracking, many businesses fail to account for costs that has happened but still it is unpaid. This oversight creates false profit pictures and dangerous cash flow surprises.

Bonuses of employees, warranty costs, and maintenance contracts with increasing prices are included in hidden costs.

3. Improper handling of multi-state tax obligations

Businesses often miss difficult tax duties that create huge duties as they are expanded beyond their home state. These accounting mistakes tax return issues can result in severe penalties and compliance problems.

- Different states have different rules about when businesses owe taxes, which means, you may owe taxes in states where they’ve never physically operated.

- Remote employee locations create payroll tax obligations in multiple states with different withholding requirements and deadlines.

- Digital services sold across state lines may trigger income tax filing requirements in customer locations.

4. Improper joint venture and partnership accounting

Complex accounting needs are the result of business collaborations and many businesses cannot manage them properly. This leads to tax and legal complications.

Revenue sharing without cost allocation, joint marketing with unequal benefits, contractor vs employee classification issues are the major problems.

5. Ignoring working capital cycle analysis

Businesses fail to understand how their working capital requirements change with growth creating scaling problems.

- New customers take longer to pay than your average (your A/R period extends from 30 to 45 days)

- You add new product lines that move slower than expected (inventory turnover drops)

- Seasonal patterns shift as you grow (cash needs change but aren’t tracked monthly)

- Your biggest customers negotiate longer payment terms, creating cash flow volatility

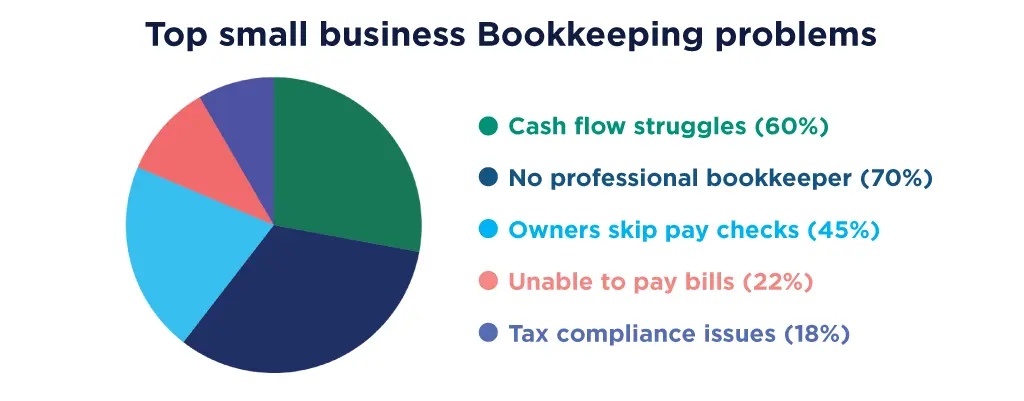

Quick stats 2025

- 60% of the small business struggles with cash flow.

- 18% of small business owners named taxes as their top challenge in 2025, reflecting ongoing legal and compliance risks.

- 22% of businesses are unable to pay basic bills.

- 70% of businesses do not has a professional bookkeeper.

- 45% of owners cannot pay themselves as they skip paychecks.

Also read: Bookkeeping and Accounting Services Guide

Consequences of Bookkeeping mistakes

Business owners fail to understand the effects of bookkeeping issues unless they face serious consequences.

According to NFIB, in 2025, 18% of U.S. small business owners named taxes as their top challenge, highlighting the growing burden of tax compliance.

Precision in financial record-keeping is the topmost priority of modern businesses. The minor data entry errors turn into significant operational challenges that affect every aspect of business performance.

Financial impact on business operations

Bad bookkeeping practices have a direct impact on cash flow predictability. When the foundational data contains errors forecasting income and expenses correctly is difficult for the businesses.

This uncertainty makes it difficult to plan for growth, manage seasonal fluctuations, or prepare for unexpected expenses.

Also, the with poor decision making in the areas of inventory, staffing or investments over time creates increased costs in opportunities affecting the profitability.

Legal and compliance consequences

The IRS maintains strict standards for business tax compliance. The failure to file penalty is 5% of the tax due for each month the return is late, up to a maximum of 25%. (Source: IRS Penalty Information)

When bookkeeping is not done properly audit risks are increased that makes the verification of the deductions difficult.

Growth and investment barriers

Banks evaluate loan applications based on financial documentation reliability. Businesses with questionable bookkeeping face higher rejection rates and less favorable terms.

Financial institutions require accurate financial statements before considering funding requests. Poor bookkeeping creates immediate red flags for lenders and investors.

How Outsourcing becomes the solution

Beyond time saving, outsourcing helps businesses get access to expert knowledge and skill that is difficult to achieve in-house.

Suppose you have a group of trained experts, who keep up with the latest technology, who are working for you tirelessly to protect your finances and spot hidden opportunities.

When regulations get stricter, mistakes becomes more costly. Outsourcing transforms the daily bookkeeping headache into a strategic advantage.

Expert skill and accuracy

With outsourced bookkeeping firms you get access to experts. These are always updated with changing regulations and best practices. High-quality service delivery is fulfilled with professional certification.

What is the golden rule of bookkeeping? To record each and every transaction accurately and completely. Professional bookkeepers follow this rule consistently without exception. This accuracy prevents the costly mistakes that plague internal bookkeeping.

Specialized software and systems provide additional accuracy improvements. Professional firms invest in advanced technology for error prevention. These tools catch mistakes before they affect financial reports.

Cost-effective solution implementation

Outsourcing is an affordable alternative as it lowers the costs significantly in comparison with hiring full-time bookkeeping staff. These services include software, training, and expertise in one package. This approach eliminates the need for internal infrastructure investment.

How to fix bookkeeping mistakes? This question becomes unnecessary with expert prevention. Error correction costs far more than proper initial recording. Outsourcing prevents mistakes rather than fixing them after occurrence.

Scalable services grow with business needs without additional hiring. Peak periods don’t require temporary staff or overtime costs. Professional firms handle volume fluctuations as part of standard service.

Advanced technology and systems integration

Modern bookkeeping requires sophisticated software and integration capabilities. Professional firms provide enterprise-grade systems at affordable costs. These systems integrate with existing business applications seamlessly.

Cloud-based access ensures real-time financial information availability. Business owners can access reports and data from anywhere. This accessibility improves decision-making speed and accuracy.

When you outsource reputable service providers they have extensive training and specializes transaction categorization. Their expertise ensures proper classification for all business transactions.

Compliance and risk management

Professional bookkeeping services include ongoing compliance monitoring. Regulation changes get implemented immediately without internal training costs. This proactive approach prevents compliance failures and penalties.

Risk assessment and fraud prevention are included in professional services. Regular audits and reviews catch problems early. These protective measures cost less than potential fraud losses.

Documentation standards exceed basic compliance requirements to provide audit-ready records. Trained bookkeepers understand what documentation satisfies various regulatory agencies. They implement systems that maintain complete audit trails while keeping businesses ahead of regulatory changes.

See related post : The Role of Outsourced Bookkeeping for Improved Efficiency

Your Trusted Outsourced Accounting Partner.

Get Started TodayKey takeaways

Common bookkeeping mistakes threaten business success more than market competition. These errors multiply over time, creating legal and financial disasters. Professional expertise prevents these costly problems effectively.

Outsourcing bookkeeping provides expert solutions at affordable costs. Professional services include accuracy, U.S. compliance, and strategic insights. This investment pays returns through error prevention and growth support.

Smart business owners choose accounting solution over internal struggles. The cost of mistakes far exceeds professional service investments.

Contact our bookkeeping experts today to protect your business success.

FAQs about common Bookkeeping mistakes

What is one of the most common bookkeeping mistakes that business owners make?

Mixing personal and business expenses represents the most frequent bookkeeping error. This mistake creates tax complications and audit risks. Professional bookkeepers maintain strict separation between personal and business finances.

How can small businesses avoid startup bookkeeping mistakes?

Startup bookkeeping mistakes decrease significantly with early professional intervention. Establishing proper systems from the beginning prevents costly corrections later. Outsourcing provides expertise without full-time employee costs.

What would you do to prevent or fix these types of mistakes?

Prevention works better than correction for bookkeeping errors. Professional outsourcing prevents mistakes through systematic processes and expertise. Early intervention costs less than error correction and penalty payments.

What could you do if you needed to enter a new transaction and weren’t sure how to categorize it?

Consult your chart of accounts first to find similar transaction types. If uncertainty remains, research industry-standard categorizations or consult with a professional bookkeeper. Document your decision-making process for consistency in future similar transactions. When in doubt, create a separate category for review rather than guessing incorrectly.

How does outsourcing help with bookkeeping mistakes in California?

Bookkeeping mistakes in California often involve state-specific compliance requirements. Professional services understand local regulations and requirements completely. This expertise prevents costly compliance failures and penalties.

What are the signs that indicate bookkeeping issues need professional attention?

Cash flow problems, tax penalties, and audit notices indicate serious issues. Missing financial reports and unclear profit margins also signal problems. Professional evaluation can assess current bookkeeping quality quickly.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.