Accounting performance is not one problem. Bookkeeping, accounts receivable, accounts payable, payroll, financial reporting, and management accounts each have their own processes, their own failure points, and their own way of affecting the business when something goes wrong.

Accounting KPIs give accountants and accounting managers a way to monitor each discipline separately. Rather than waiting for a cash flow gap or a tax filing issue to surface, the right key performance indicators show where a function is underperforming before it affects the business.

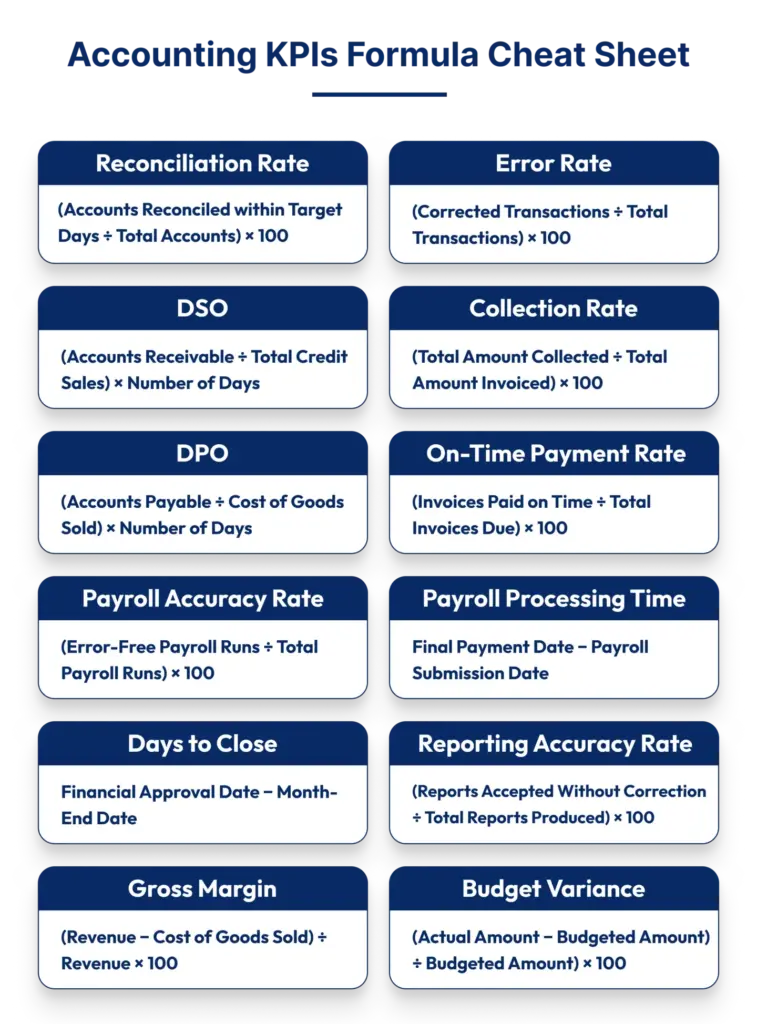

This guide covers 12 accounting KPIs across six core disciplines, with formulas, benchmarks, and ownership guidance for each.

Key takeaways

- Accounting KPIs measure whether the accounting function is working correctly, not whether the business is profitable.

- Each discipline has its own indicators. A payroll problem looks different from a collections problem.

- Accounting benchmarks are directional, not universal. Your own trend over time is more reliable than any industry average.

- Accounting problems show up in the numbers before they reach the bank account.

- A KPI without an assigned owner is not being managed.

What are Accounting KPIs?

Accounting KPIs are measurable indicators used to assess the performance of specific accounting functions. They provide a structured way to monitor the effectiveness of different accounting activities.

Since accounting responsibilities are divided across multiple disciplines, the KPIs used to measure performance vary by function. The following disciplines form the foundation of most accounting departments.

| Discipline | Primary Responsibility | Typical Owner |

|---|---|---|

| Bookkeeping | Recording, categorizing, reconciling | Bookkeeper |

| Accounts Receivable | Invoicing, collections | AR specialist or bookkeeper |

| Accounts Payable | Vendor payments, scheduling | AP specialist or bookkeeper |

| Payroll | Compensation, tax withholding | Payroll specialist |

| Financial Reporting | Month-end close, statements | Controller or accounting manager |

| Management Accounts | Internal performance reporting | Controller or CFO |

Important note about benchmarks: Benchmarks below are directional and should be interpreted against your industry, payment terms, and internal trends.

Bookkeeping KPIs

Every other accounting function depends on bookkeeping being accurate. Transactions recorded incorrectly, expenses placed in the wrong account, or reconciliations running behind do not stay contained. Errors flow into financial reports, tax filings, and cash flow decisions.

Bank Reconciliation Timeliness

Reconciliation matches accounting records against actual bank and credit card statements. It must happen within a defined number of days after each month closes, before any report is produced from those numbers. 💡Formula: (Accounts reconciled within agreed days of month-end ÷ Total accounts) × 100

Completing reconciliation close to month-end makes every report that follows more reliable. A business owner tracking this needs one data point: how many days passed between month-end and confirmed accurate books.

- Completing all accounts within 5 business days of month-end is commonly considered good practice, though no universal standard exists for this

- Up to 10 business days is generally seen as acceptable

- Beyond 10 business days: any report produced in that window is working off unverified numbers

The bookkeeper owns this. The accounting manager reviews it monthly.

Transaction Error Rate

This measures the percentage of transactions recorded incorrectly in a given period, including wrong category, duplicate entry, or wrong amount. 💡Formula: (Corrected transactions ÷ Total transactions processed) × 100

Errors in transaction categorization affect the profit and loss statement directly. A misrecorded expense can misstate taxable income, which can create problems during tax filing and financial review.

The error rate should stay consistently low and trend downward over time as review processes improve. A rising rate month over month points to one of three things:

- A training gap on the bookkeeper’s side

- A volume increase the current review process cannot handle

- A quality check that is not catching mistakes early enough

For example: A business processing 800 transactions a month at a 3% error rate has 24 entries requiring correction each month. At that volume, errors are not occasional. They are a recurring cost in staff time and risk.

Accounts Receivable KPIs

Revenue on paper and cash in the bank are not the same thing. The gap between them lives in accounts receivable.

A business can be profitable by every measure and still face cash problems if collections are not running on schedule.

Days Sales Outstanding

DSO measures the average number of days between issuing an invoice and receiving payment. Days Sales Outstanding (DSO) is widely used to assess how efficiently a business collects receivables. A lower DSO means cash comes in faster, which supports liquidity. 💡Formula: (Accounts Receivable balance ÷ Total Credit Sales) × Number of days in the period

In many businesses, a DSO below 45 days may be viewed as reasonable, but the more useful benchmark is how it compares with your payment terms and past trend., though it varies by industry and business size. The most useful benchmark is your own payment terms:

- Terms Net 30, DSO 32: collections are broadly on track

- Terms Net 30, DSO 55: 25 days of cash is sitting beyond the agreed deadline

- DSO rising consistently over several months: the collections process needs attention

The AR specialist or bookkeeper managing collections owns this, reviewed monthly.

For example: A business with $120,000 in outstanding receivables and $80,000 in monthly credit sales has a DSO of approximately 45 days. If payment terms are Net 30, that 15-day gap is where the collections conversation starts.

Collection Rate

Where DSO measures how long collections take, collection rate measures how much invoiced revenue is actually being recovered. 💡 Formula: (Total amount collected ÷ Total amount invoiced) × 100

A declining collection rate over consecutive months points to one of three things:

- Write-offs are increasing

- Disputes are going unresolved

- Follow-up after an invoice becomes overdue is not consistent enough

| AR Metric | What It Measures | Warning Sign |

|---|---|---|

| Days Sales Outstanding | How long invoices take to get paid | Rising DSO month over month |

| Collection Rate | How much invoiced revenue is actually recovered | Rate declining over consecutive months |

A consistently high collection rate is usually expected, but the most useful benchmark is whether the rate is stable or improving over time.

Accounts Payable KPIs

Paying vendors accurately and on time without tying up unnecessary cash requires balance. Paying too early reduces liquidity. Paying late can result in fees, tightened credit terms, or prepayment requirements. Both outcomes are measurable.

Days Payable Outstanding

DPO measures the average number of days a company takes to pay its bills and invoices to trade creditors. It reflects how long a business holds its cash before meeting payment obligations. 💡 Formula: (Accounts Payable balance ÷ Cost of Goods Sold) × Number of days in the period

For service businesses with limited cost of goods sold, DPO should be evaluated against vendor payment terms and cash flow patterns.

A higher DPO can indicate that a business is managing its cash efficiently. However, a DPO that stays consistently beyond agreed vendor terms points to either a cash flow problem or a payment process that is not working. The right benchmark is your own vendor payment terms:

- Paying consistently within terms: healthy position

- Paying well ahead of terms: cash leaving earlier than necessary

- Paying past terms regularly: vendor relationships and credit terms are at risk

On-Time Payment Rate

This measures the percentage of vendor invoices paid by or before the due date. 💡Formula: (Invoices paid on time ÷ Total invoices due) × 100

A consistent drop in this rate points to one of three things:

- A cash flow problem affecting the ability to pay on schedule

- Invoices not being entered into the system on receipt

- An internal approval process creating payment delays

Payroll KPIs

Under the Fair Labor Standards Act, covered nonexempt employees must receive overtime pay of at least 1.5 times their regular rate for hours worked over 40 in a workweek

According to the IRS, payroll tax deposits follow either a monthly or semi-weekly schedule, determined by the employer’s reported tax liability in the lookback period.

Errors in either area carry regulatory consequences. Payroll KPIs are reviewed after every run, not monthly.

Payroll Accuracy Rate

This tracks the percentage of payroll runs completed without errors, including incorrect hours, missed deductions, wrong tax withholdings, or omitted adjustments. 💡Formula: (Error-free payroll runs ÷ Total payroll runs) × 100

- An underpayment is a potential FLSA violation

- An incorrect withholding creates an IRS filing issue requiring correction and documentation

- Payroll accuracy should stay as close to 100% as the process allows

Investigate any error immediately. Do not treat it as routine.

For example: A business running weekly payroll for 40 employees at a 2% error rate will have roughly one payroll error every two and a half weeks, approximately 20 corrections over a year, each requiring employee communication and possible IRS adjustment.

Payroll Processing Time

This measures how long each payroll run takes from data submission to payment reaching employees. 💡Formula: Date of final payment − Date payroll data was submitted (tracked per run, averaged monthly)

According to IRS employment tax due dates, semi-weekly depositors must deposit employment taxes by the following Wednesday for payments made on Wednesday, Thursday, or Friday, and by the following Friday for payments made on Saturday through Tuesday.

A process that consistently runs long creates risk of missing that window. The cause is usually one of three things:

- Timesheets being submitted late

- Data requiring manual correction before processing can begin

- A workflow that has not been updated to match current payroll volume

Financial Reporting KPIs

Financial reporting is where the accounting function produces its output: the statements, the close, the numbers a business owner or lender actually uses. These accounting and financial reporting KPIs measure whether that output is on time and reliable.

Days to Close

This measures how many business days after month-end it takes to produce finalized financial statements. 💡Formula: Date final financials approved − Last day of the month (in business days)

When financials are consistently late, decisions are being made on old information. A shorter close cycle means more time between seeing the numbers and needing to respond to them. The controller or accounting manager owns this, tracked every month.

- In many businesses, completing reconciliations within 5 business days of month-end is considered good practice, though the right target depends on reporting needs and team capacity

- Up to 10 business days is generally seen as acceptable

- Beyond 15 business days may indicate a process, staffing, or systems issue that needs review

Reporting Accuracy Rate

This measures the percentage of financial reports delivered without material errors or corrections after issue. 💡Formula: (Reports accepted without correction ÷ Total reports produced) × 100

Any report requiring restatement after delivery is a quality event. If it happens more than once in a quarter from the same source, the review process before reports are issued needs to change.

Management Accounts KPIs

Management accounts are internal financial reports produced throughout the year to give decision-makers a current picture of business performance. These management accounting KPIs make those reports actionable rather than just historical.

Gross Profit Margin

Investopedia defines gross profit margin as the percentage of revenue remaining after subtracting the direct costs of producing goods or delivering services. 💡Formula: (Revenue − Cost of Goods Sold) ÷ Revenue × 100

Investopedia notes that gross profit margin varies significantly by industry, and comparing against others in the same sector is more meaningful than applying a universal number.

NYU Stern’s US industry margin dataset shows the range across sectors, from single-digit margins in retail to above 60% in software. The more useful internal measure is the trend:

- Stable margin over consecutive periods: costs and pricing are in balance

- Declining margin without a clear explanation: costs are rising faster than revenue, or pricing has not kept pace with delivery costs

Budget vs Actual Variance

This measures the percentage difference between planned and actual figures across revenue and expense categories. 💡Formula: ((Actual Amount − Budgeted Amount) ÷ Budgeted Amount) × 100

A single-period variance can be an anomaly. Consistent variance in the same categories over multiple months points to one of two things:

- The budget was built on assumptions that do not reflect how the business actually operates

- Spending in those areas is not being monitored between reporting periods

The controller or CFO owns this, reviewed monthly as part of the management accounts pack.

Individually, each KPI measures a specific accounting activity. Taken together, they show how effectively the accounting function supports the business. Understanding how these measures are calculated helps ensure that performance is assessed consistently across each area.

Different KPIs require attention at different intervals. Payroll metrics often need review after every run, while most bookkeeping and reporting measures are assessed monthly. Assigning ownership ensures that issues receive attention before they affect business performance.

KPI Review Frequency

| KPI | Discipline | Review Frequency | Owner |

|---|---|---|---|

| Bank Reconciliation Timeliness | Bookkeeping | Monthly | Accounting manager |

| Transaction Error Rate | Bookkeeping | Monthly | Accounting manager |

| Days Sales Outstanding | Accounts Receivable | Monthly | AR specialist or bookkeeper |

| Collection Rate | Accounts Receivable | Monthly | AR specialist or bookkeeper |

| Days Payable Outstanding | Accounts Payable | Monthly | AP specialist or bookkeeper |

| On-Time Payment Rate | Accounts Payable | Monthly | AP specialist or bookkeeper |

| Payroll Accuracy Rate | Payroll | After every run | Payroll specialist |

| Payroll Processing Time | Payroll | After every run | Payroll specialist |

| Days to Close | Financial Reporting | Monthly | Controller or accounting manager |

| Reporting Accuracy Rate | Financial Reporting | Monthly | Controller or accounting manager |

| Gross Profit Margin | Management Accounts | Monthly | Controller or CFO |

| Budget vs Actual Variance | Management Accounts | Monthly | Controller or CFO |

Your Trusted Outsourced Accounting Partner.

Get Started TodayConclusion

Tracking these accounting department KPIs does not require complex software or a large team. It requires knowing which discipline each KPI belongs to, who is responsible for it, and which direction it should be moving in. Regular monitoring helps identify issues early and supports better decision-making.

If your accounting function is newly built or outsourced, start with one or two KPIs from each discipline. The goal is not to measure everything at once. It is to have enough visibility that nothing significant goes unnoticed.

If these KPIs are difficult to track consistently, outsourcing accounting support can help create ownership and reporting discipline.

Outbooks helps US businesses manage bookkeeping, payroll, reporting, and other accounting functions. Contact us at +1 386 251 5318 or info@outbooks.com.

FAQs

What is the difference between an accounting KPI and an accounting metric?

A metric tracks activity whereas a KPI measures performance against a specific target. Every KPI is a metric, but not every metric is a KPI.

How do I set a target for an accounting KPI if no industry benchmark exists?

Use your own historical data as the baseline. Track the number for two to three months, establish your current average, then set a realistic improvement target from there.

Can outsource accounting teams be held to the same KPIs as in-house teams?

Yes, DSO, payroll accuracy rate, reconciliation timeliness, and days to close apply regardless of whether the function is in-house or outsourced.

If my DSO is high, does that mean my bookkeeper is underperforming?

Not necessarily, DSO is owned by the AR function, not bookkeeping. A high DSO points to a collections process problem, not a recording or reconciliation issue.

How many accounting KPIs should a small business realistically track?

One to two KPIs per discipline is a practical starting point. Tracking twelve numbers across six disciplines is manageable without becoming difficult to maintain.

What should happen when an accounting KPI is consistently missed?

Identify whether the issue is a process problem, a volume problem, or a personnel problem. A KPI missed once is a data point. Missed three months in a row, it is a pattern that needs a direct conversation.

What is a good accounting KPI benchmark?

A good accounting KPI benchmark is one that reflects your business size, industry, and processes. Consistent improvement against your own historical performance is often more useful than a universal target.

How can accountants track KPIs efficiently?

Accountants can track KPIs efficiently through accounting software, automated dashboards, and regular performance reviews. Monitoring trends consistently helps identify issues early and supports better financial decision-making.

Parul is a content specialist with expertise in accounting and bookkeeping. Her writing covers a wide range of accounting topics such as payroll, financial reporting and more. Her content is well-researched and she has a strong understanding of accounting terms and industry-specific terminologies. As a subject matter expert, she simplifies complex concepts into clear, practical insights, helping businesses with accurate tips and solutions to make informed decisions.